Time after time in recent years, the ECB has prevented the European economy from collapsing. These interventions gave politicians time to solve fundamental governance issues but this also fuelled financial bubbles, led to wealth redistribution without a political mandate and the politicisation of the central bank. As these issues will increase with each successive intervention in the future, the politicians really have to solve the next crisis themselves.

In recent years, the European Central Bank (ECB) has intervened on multiple occasions to keep the currency union together. The ECB has generously provided loans to commercial banks since 2008. In 2012, the ECB reconfirmed its commitment by declaring it would support countries should this prove necessary.[79]

With these measures, the Central Bank bought time for the politicians to sort things out – time the politicians desperately needed, because they lacked the tools to enact a swift resolution. A proper safety net for member states in budgetary difficulties was not in place, nobody had a really clear overview of the health of the systematically important banks in Europe, and no-one had the authority to intervene on the basis of this information. These flaws in the governance of the currency union led to a situation where a default of Greece, a country that accounts for just 2 percent of the total eurozone GDP, could lead to the dissolution of the eurozone.

Neither the national governments nor the European Commission could solve the issue. In an incomplete union where the member states are in charge, these governance flaws cannot be solved by an executive order. Responsibilities have to be negotiated and demarcated, institutions have to be set up and organised at an European level, and the member states have to find their own place in, and accept, the new reality.

The ECB was really the only institution capable of intervening in order to keep the currency union together. As ECB’s President Mario Draghi put it: “I do not think we are unbiased observers, we think the euro is irreversible.”[80] Nevertheless, the Central Bank has always motivated its interventions by the need to have financial conditions in which monetary policy help to stabilise prices in the real economy. This is the Bank’s mandate and it is on this basis it should operate.

Inadequate utilisation of this respite period

This period of respite was put to some good use: the European Stability Mechanism can save small member states; supervision at a European level of the systematically important banks was assigned to the ECB; and the Eurogroup was made permanent in nature.

However, the steps taken are not sufficient. A safety net for the larger member states is lacking, the banking union has not been completed – for instance, there is no European deposit insurance scheme and it is unclear who acts as the lender of last resort – and, more important in terms of European budgetary policy, there is no stabilisation mechanism.

Due to the insufficiency of the steps taken, a debt-deflationary spiral became likely in early 2015. Had the governments of the member states set up a proper safety net, a banking union and a European stabilisation mechanism, they would have created room for private-sector growth. Without these measures European households and firms felt compelled to reduce their expenditures respectively their investments in order to create the means to service their debt obligations. This reduction in economic demand led to a downward pressure on prices and accordingly to an increase of the debt obligations in real terms.[81]

Side effects of quantitative easing

In response, the ECB stepped in once more: it bought time by providing very generous levels of liquidity. Once more, the ECB’s policy was successful, as a debt-deflationary spiral is no longer a threat. However, it did so at substantial cost: in the Bank’s latest intervention, the time that had been bought was not accompanied by political action. As a result, since 2015 the macro-economic governance of the Union has seen little improvement.

Quantitative easing (QE) has however had significant side effects. It laid the foundations for new financial and economic problems since the low interest rates and the abundant liquidity are forcing investors to take more risk. As a result, the prices for real estate, shares and bonds are rising to record highs. The question is: do these prices rely on economic fundamentals or has a financial bubble been created? While bubbles can only be identified with certainty in retrospect, the risk is very real.

What’s more, a political narrative supporting current policy is lacking. This is dangerous. The artificially low interest rates are putting pension benefits under pressure, which provide a fertile ground for 50Plus, the pensioners political party in the Netherlands; the lack of risk sharing in the currency union ensures that the narratives put forward by Syriza in Greece and the Front National in France attract larger audiences; and in addition the growing wealth inequalities – fuelled by the rise in asset prices – is providing ammunition for populists on both sides of the political spectrum.

Consequences for the Central Bank

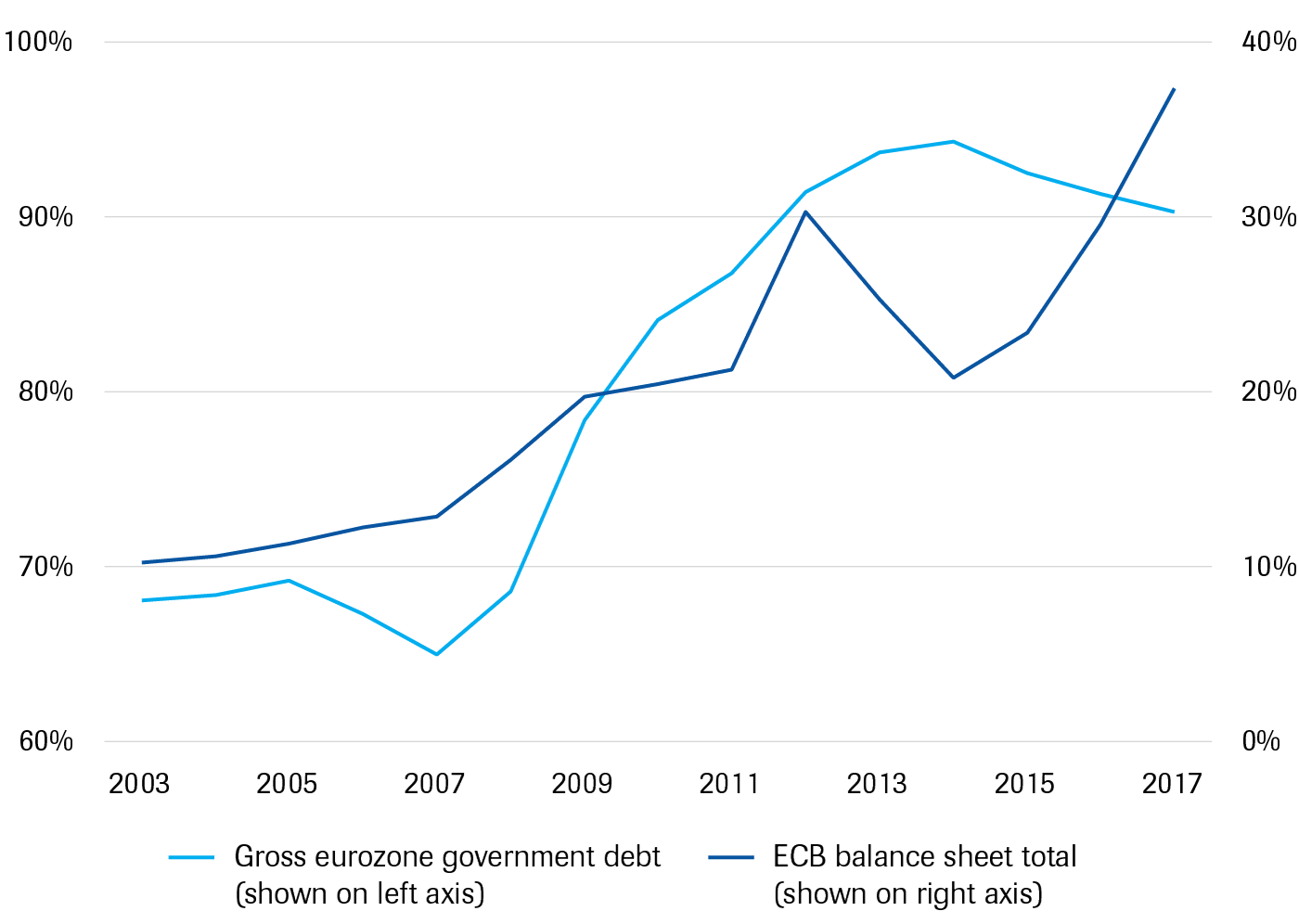

The ECB is actually providing monetary financing. This is not altered by the fact that the ECB has not bought government bonds from the member states directly. Figure 1 below illustrates that from 2003 onwards, both the gross national debt of the Eurozone countries and the ECB’s balance sheet total have risen by an amount equal to 25 percentage points of the Eurozone’s total GDP, and have done so at about the same speed. This illustration would have looked just the same if the eurozone countries had sold these bonds directly to the ECB.

Figures for debt and balance sheet total are annual averages.

Source: Gross national debt and GDP figures are from Eurostat, balance sheet total figures are from the ECB.

Monetary financing is risky. First, it makes the Central Bank part of the European political process. In practice, the ECB can now decide the political future of member states. A shining example of this, is the letter that ECB President Trichet sent in 2011 to the Italian government. It ultimately led to Berlusconi’s departure.[82]

Secondly, monetary financing is, also at the national level, no longer ‘neutral’. In other words, a central bank that deploys monetary financing must take decisions that are traditionally reserved for politicians, even though central bankers have no electoral mandate to do so. A shining example of this is the increase in asset prices due to QE and subsequent wealth redistribution.

Both issues emerge in monetary financing. Which (corporate or other and from what country) bonds will the ECB buy and which will it not buy, and what are the consequences of this?

In this respect the main danger lies in the consequences this might have for its independence and thus for its credibility and for its options as far as restraining inflation in the medium term is concerned. By the way, while this spectre haunts the more ordoliberal-oriented economists, central bankers seem less concerned.[83]

Doing nothing is not an option

So, what would be the sensible thing to do now? There are three obvious options: Doing nothing; accelerated reduction of government debt and central bank balances; and taking political responsibility. Let’s look at all three in turn.

Currently, the economy is recovering strongly in the eurozone. This is why doing nothing and biding one’s time may seem a good strategy. If the eurozone succeeds in unwinding its balance sheets of QE in an orderly fashion and if member states use their improved financial position to repay their debts then the ECB’s balance sheet total and debt levels can return to the pre-crisis positions.

However, biding one’s time is not a good strategy. It would take a very long time for the size of the balance sheet to contract. Given 1.75 percent economic growth and 2 percent inflation per year it would take until the year 2046 before the economy has grown so much that the balance sheet total of the ECB relative to GDP will reach its pre‑crisis level.[84]

Well before 2046, a recession might be due, which might be accompanied by a financial crisis. Recessions generally occur every four to eight years and recessions accompanied by a financial crisis every fifteen to twenty years.[85] The financial crisis occurred in 2007 and the ‘double dip’ in 2013.

In the event of a new recession, the member states’ governments and the ECB will be able to do little apart from creating more debt to be financed directly or indirectly by means of monetary financing. The interest rate, which was lowered when the economy needed to be stimulated up to 2008, is unavailable as a tool for macroeconomic stabilisation. It currently stand at zero percent and cannot be reduced further. Moreover, the neutral interest rate (i.e. the rate in an economy that is neither depressed nor booming) has been declining for many years now, making it unlikely that the interest rate will be positive even if the economy would perform very well in the future.[86]

Additional QE will feed the flames of a financial bubble and will further increase political pressure. The latter will become pressing when the ECB has bought the government bonds that are available for sale. Will it buy risky corporate bonds or shares and, if so, of which companies and from which member states? Given the large effects on the value of those assets if the ECB does buy them, these will be important questions.

Difficult to achieve a sufficiently rapid reduction

An economically advisable solution would be an accelerated reduction of both the size of the ECB’s balance sheet and the national debts in the Eurozone, and to link this to measures that eliminate the effective lower bound for the Central Bank interest rate. This allows the rate to be reduced further should this prove necessary to stimulate the economy.

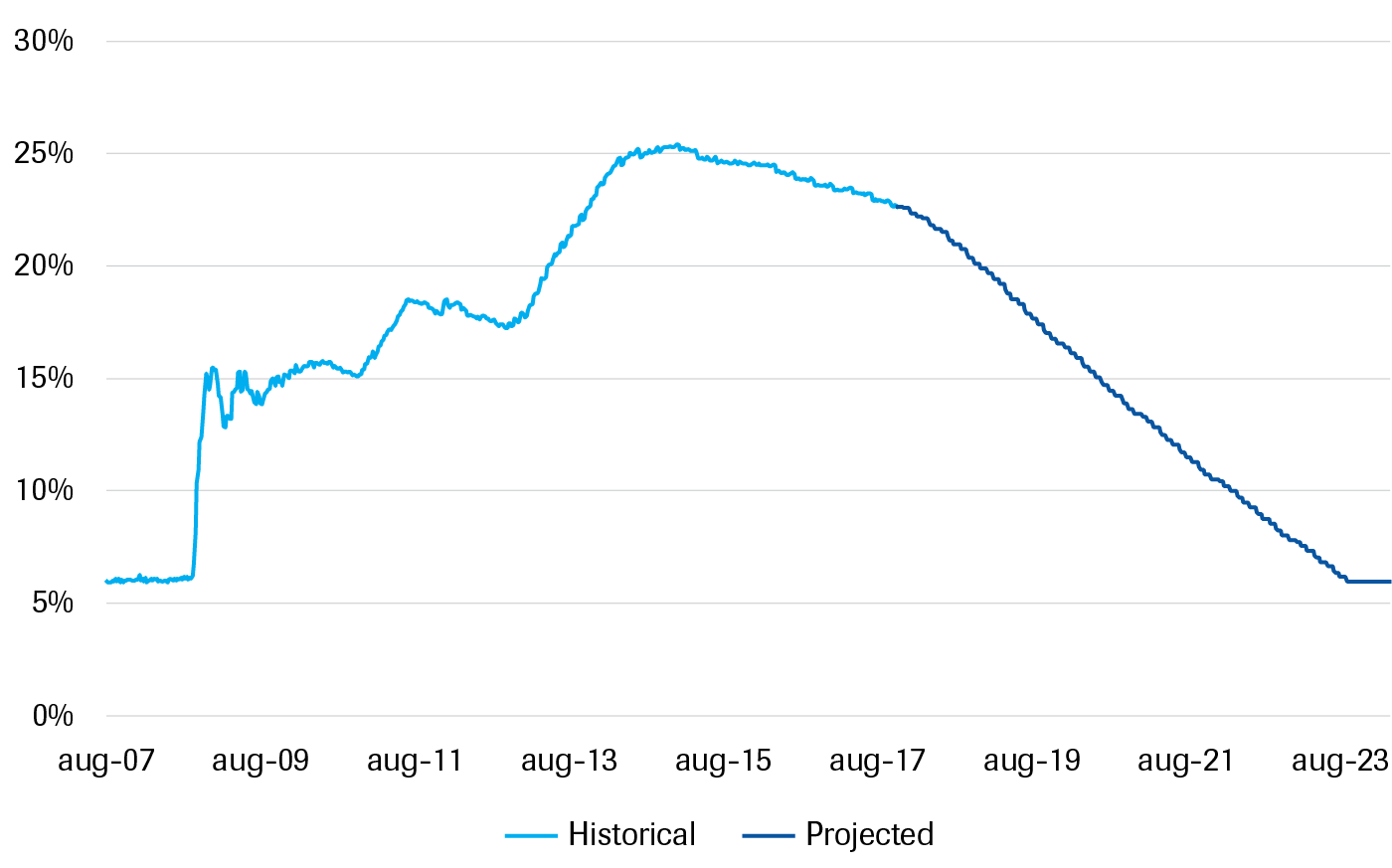

I doubt whether this reduction can proceed quickly enough. A comparison with the United States helps to illustrate this point. Last November, the Federal Reserve (Fed) started its own programme of reduction. According to the current plan,[87] in five and a half years’ time its balance sheet total will again be at its pre-crisis level (see Figure 2).

In contrast, in Europe the size of the balance sheet is still increasing – note that QE was recently slowed down, not halted,[88] and that in Europe, unlike in the US, political considerations can delay this reduction process. The decision to start with the QE programme has been influenced by the stabilising effect the programme was supposed to have on Southern Europe, and this will likely be the case for any discussion about ending this programme too.

A rapid reduction plan in Europe would thus likely take a lot more than five and a half years. In the meantime, a recession could derail both the economy and the aforementioned reductions ‘just like that’, thereby leading to adverse effects such as the blowing of financial bubbles, the lack of political narrative and the risks posed to the Central Bank’s autonomy.

Source: data from FRB (Federal Reserve Bank of) St. Louis + own calculations (details available).

Political responsibility

Hence an economic solution is unlikely to succeed, and this is because the downside of the current policy mix originates from the fact that it was the Central Bank – and not politicians – which had to defuse the crisis. To accomplish this task the ECB used the tools at its disposal, which do not include risk-sharing between countries or the remission (i.e. forgiving) of household debt. Had these options been chosen, the Union’s economy would probably be in much better shape. These, however, were decisions that could only have been taken by politicians, not by central bankers.

Opting for a political solution may be late, but it is not too late. A political solution entails that politicians take responsibility for macro-economic policy, i.e. organize macro-economic governance at a European level, and pledge to use it to stabilise the Union when the next crisis occurs. If they do so, it will be the politicians who will have to decide on the degree of risk sharing, on the degree to which incomes are distributed and on the way in which this has to be implemented in practice.[89]

There is a clear economic benefit to this. In the hands of politicians, options such as risk sharing between countries and the remission of household debt will be given equal consideration to issuing more public debt and financing it monetary. The consequence of all this would however be that the politicians involved would also have to bear responsibility for the policies that are pursued now as well as in the future.[90]

This has both economic and political benefits. The electorate will find it harder to vote for populists if elected politicians can actually implement their economic policies. A vote ensuing more consequences will be cast after more serious consideration. What’s more, the debate about the politicisation of the ECB will become obsolete, if the politicians do their job.

Depolitisation of the ECB is good for price stabilisation. The ECB is currently pursuing policies on its own authority that have a major impact on the real economy. While it is true the ECB is pursuing these policies with the implicit support of the majority of the member states, a political climate change might turn this support into opposition. Were this to happen, the ECB would be dealt a blow from which it may have a hard time recovering. It is likely this impacts price stability as well.

About the authors

Jasper Lukkezen is Editor-in-chief of Economisch Statistische Berichten (ESB), a Dutch journal on policy economics. He furthermore serves as assistant professor in macroeconomics at Utrecht University. He has broad experience as a policy advisor on fiscal policy and macroeconomic stability.