This chapter sets out to explore the economic impact of Syrian crisis in Lebanon and the narratives surrounding it among Lebanese actors and donors. Two economic narratives are of particular relevance for the effectiveness of the protection in the region agenda:

the narrative stressing the lack of export opportunities as a driving factor behind Lebanon’s slowing economic growth, which is important for understanding the attitudes of Lebanese actors in negotiations on aid modalities with key donors.

the narrative of the negative impact of the physical presence of refugees on the country’s economy in general, and infrastructure in particular, that frames the discussions on aid.

It is beyond the scope of this chapter to provide anything resembling a comprehensive analysis of the full economic impact of refugee presence or Syrian crisis on Lebanon. The Lebanese political economy is not only reproduced through its informality[32] and clientelistic service allocation but also through the narratives it creates to explain them. Reliable data is impossible to come by on most topics because such data could jeopardise the different sectarian narratives. In many cases data is either not produced (e.g. an updated population census), or of questionable quality, making it subject to various interpretations and contentious debate (e.g. financial reporting, such as the national accounts, balance of payments, labour market assessments, etc.).[33] The lack of reliable data is so acute that the World Bank’s blueprint for economic reform states that tackling it is a priority.[34] The analysis that informs this chapter is subject to similar data constraints, but nevertheless serves to highlight the strong role of Lebanese narratives framing the impact of the Syrian crisis.

2.1 The Syrian war and its economic fallout

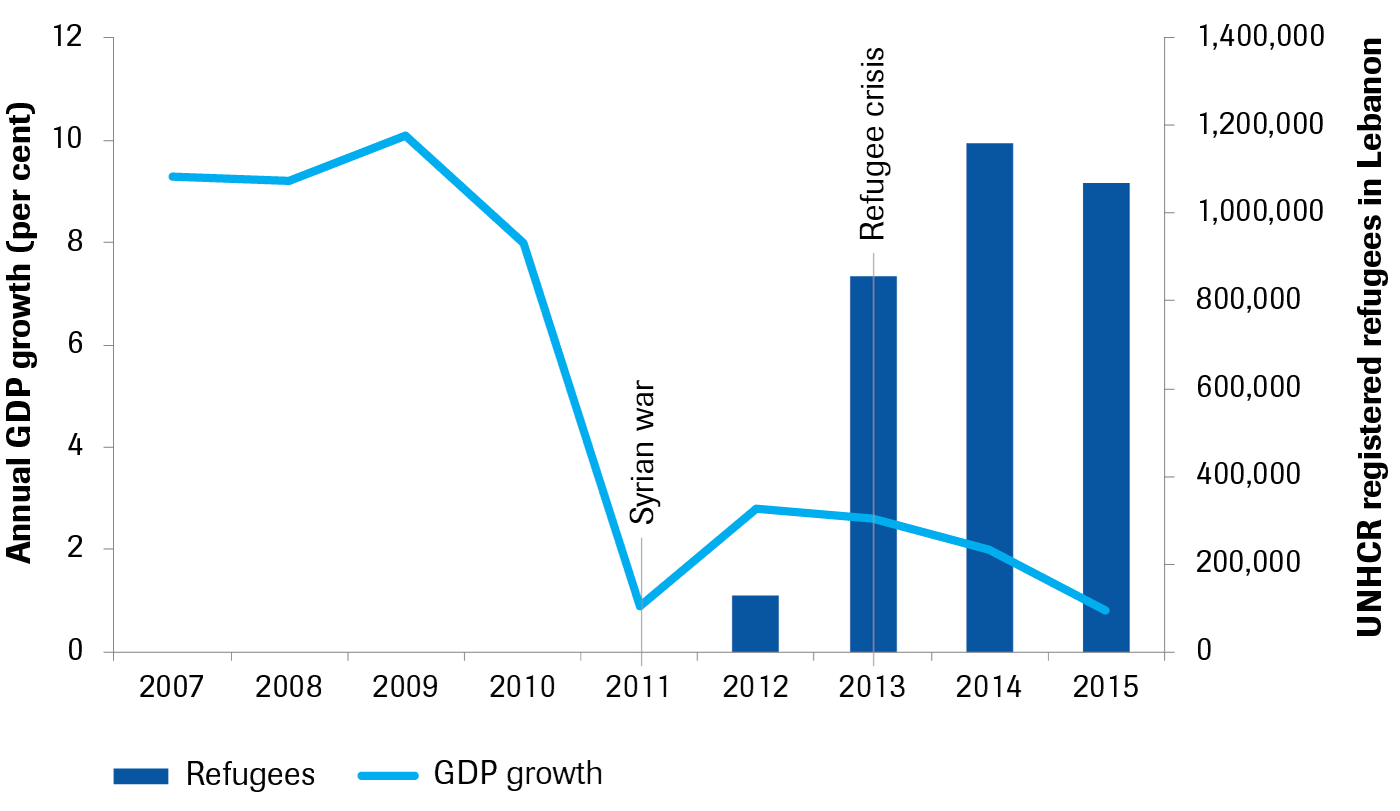

While Lebanon’s economy has undoubtedly been affected by the Syrian war and the subsequent influx of refugees, our findings confirm the growing consensus that not all of the country’s current economic woes can be attributed to these events. What is more, the impact of the Syrian war and refugee crisis should not be considered as a single event. Lebanon’s GDP growth rate dropped sharply at the onset of the Syrian war, while the large influx of refugees did not commence until over a year later (see figure 4). In the following pages we will explore the impact of each event in turn.

In 2011 the growth of the Lebanon’s economy, which in previous years had been oscillating between 8 and 10%, took a plunge, slowing to less than 1%.[36] This sudden slowdown coincided with the onset of the Syrian war and a parallel was easily drawn. The correlation between the two events was frequently linked to reduced export opportunities for the Lebanese, effectively externalising the cause of the decline . Later, this served as the basis for an appeal to widen export opportunities from Lebanon to the EU.

The argument around reduced export opportunities was couched in two main claims: 1) export to Syria declined (especially for agricultural goods) as the Syrian market collapsed; and 2) exports to other important trading partners (Turkey and the Gulf) fell as transport routes through Syria became inaccessible.

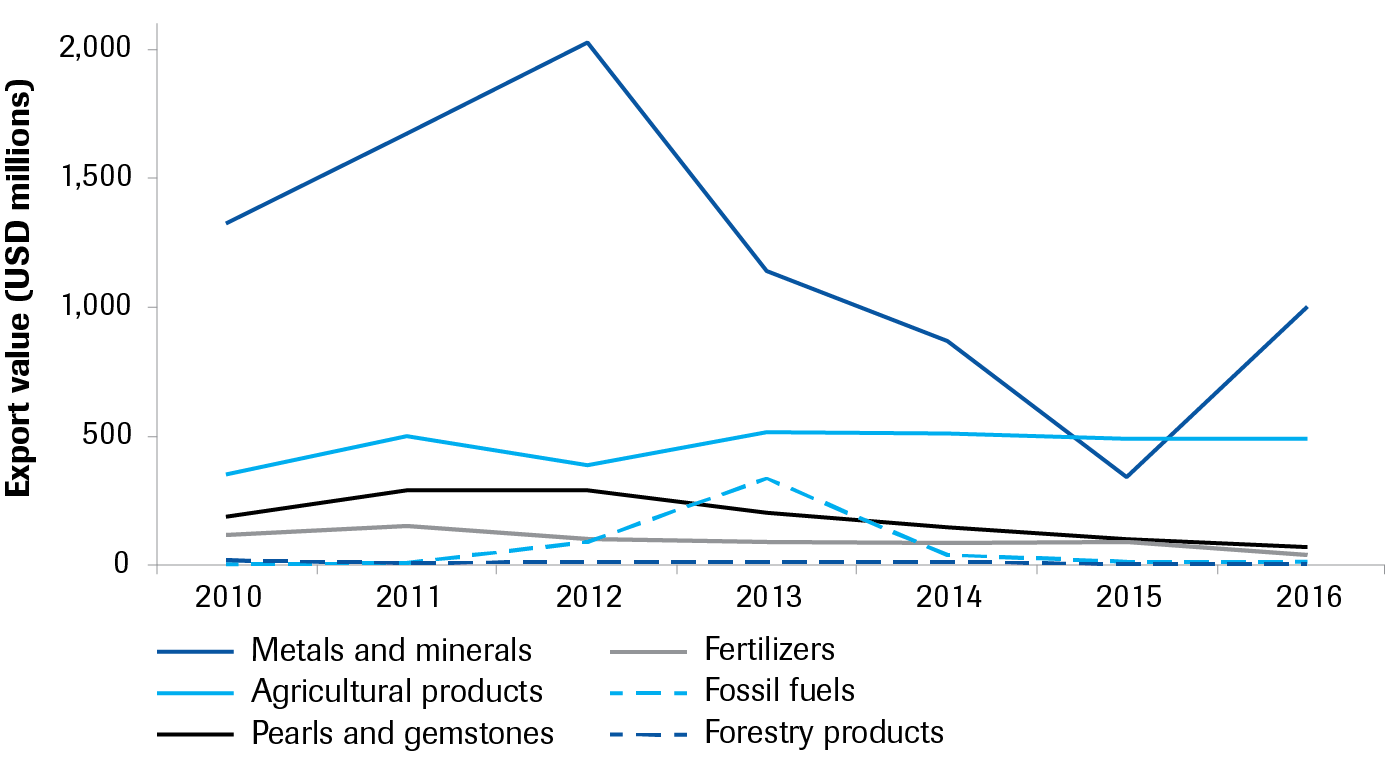

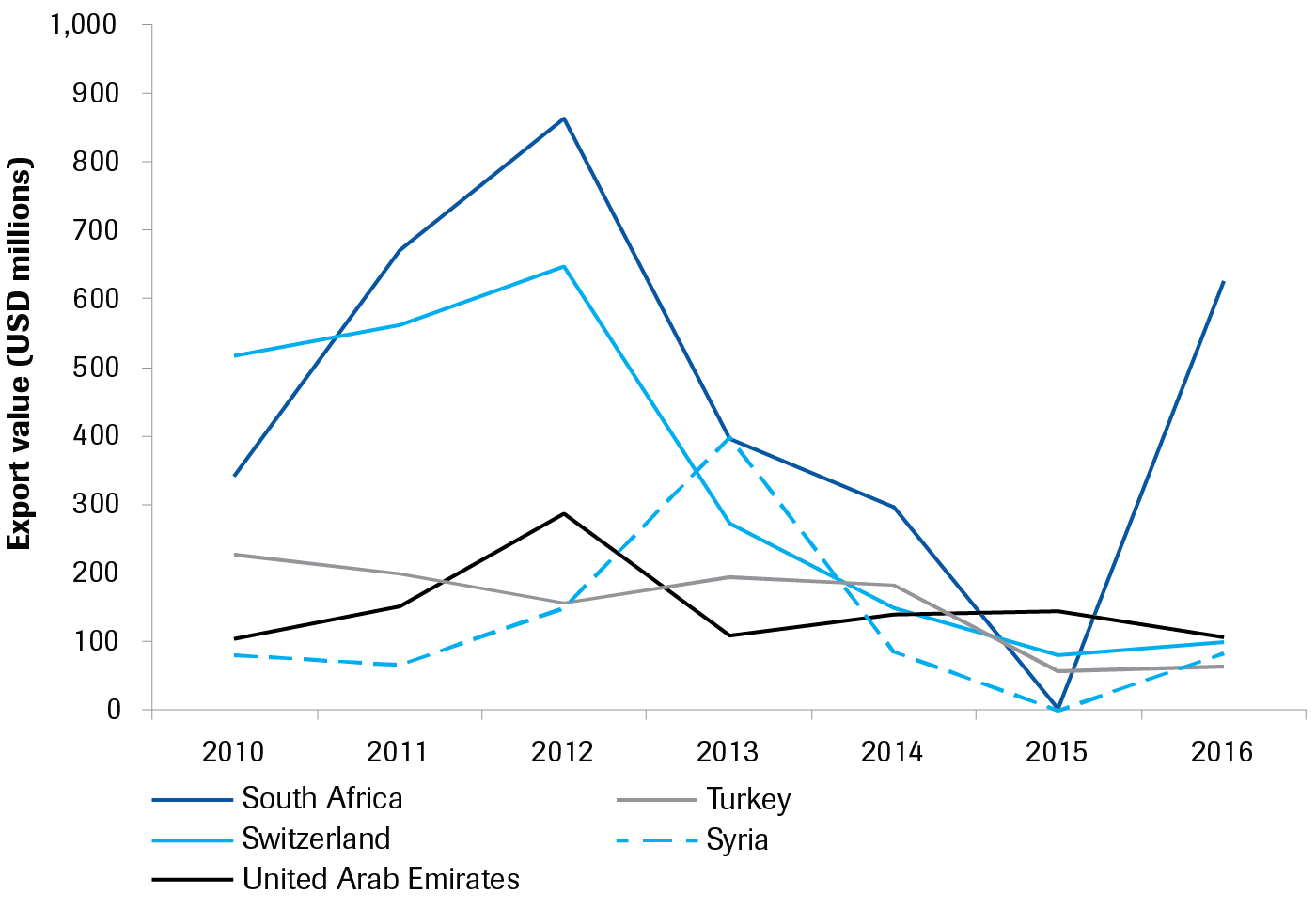

As regards the first claim, a closer look at Lebanese exports does indeed confirm that Syria consistently ranks among the top 10 export destinations of Lebanese goods, yet agricultural exports to Syria are a relatively minor component of total exports. It also reveals however, that exports of natural resources to Syria increased from 2011 to 2013, as agricultural exports remained relatively stable and a new stream of refined oil and oil products developed. Natural resource exports dropped significantly following 2013 as oil-related earnings dropped once again, with agricultural exports forming the main export at comparable levels as before (with the exception of 2015). However, it should be noted that exports to Syria (on average USD 123 million between 2010 and 2016) are a minor flow compared to an overall export of natural resources averaging USD 2 billion. The export of metals and minerals (mainly gold) to South Africa and Switzerland formed a far more significant component of the Lebanese export earnings (USD 672 million and USD 562 million in 2011 respectively), and declined significantly in this period (see figures 5 and 6).[37] The high salience of exports to Syria may be based more on the importance of agricultural districts in Lebanese politics than on an actual reduction of agricultural exports to Syria.

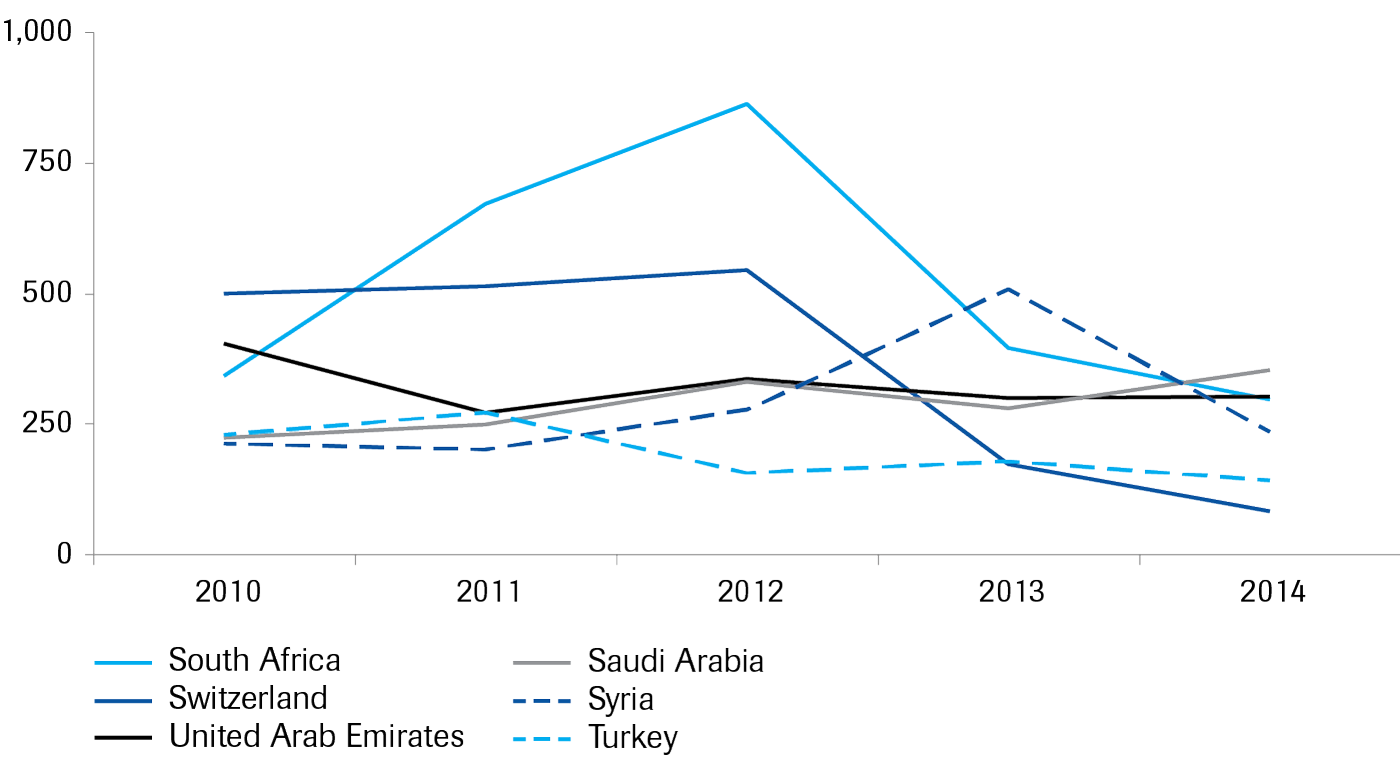

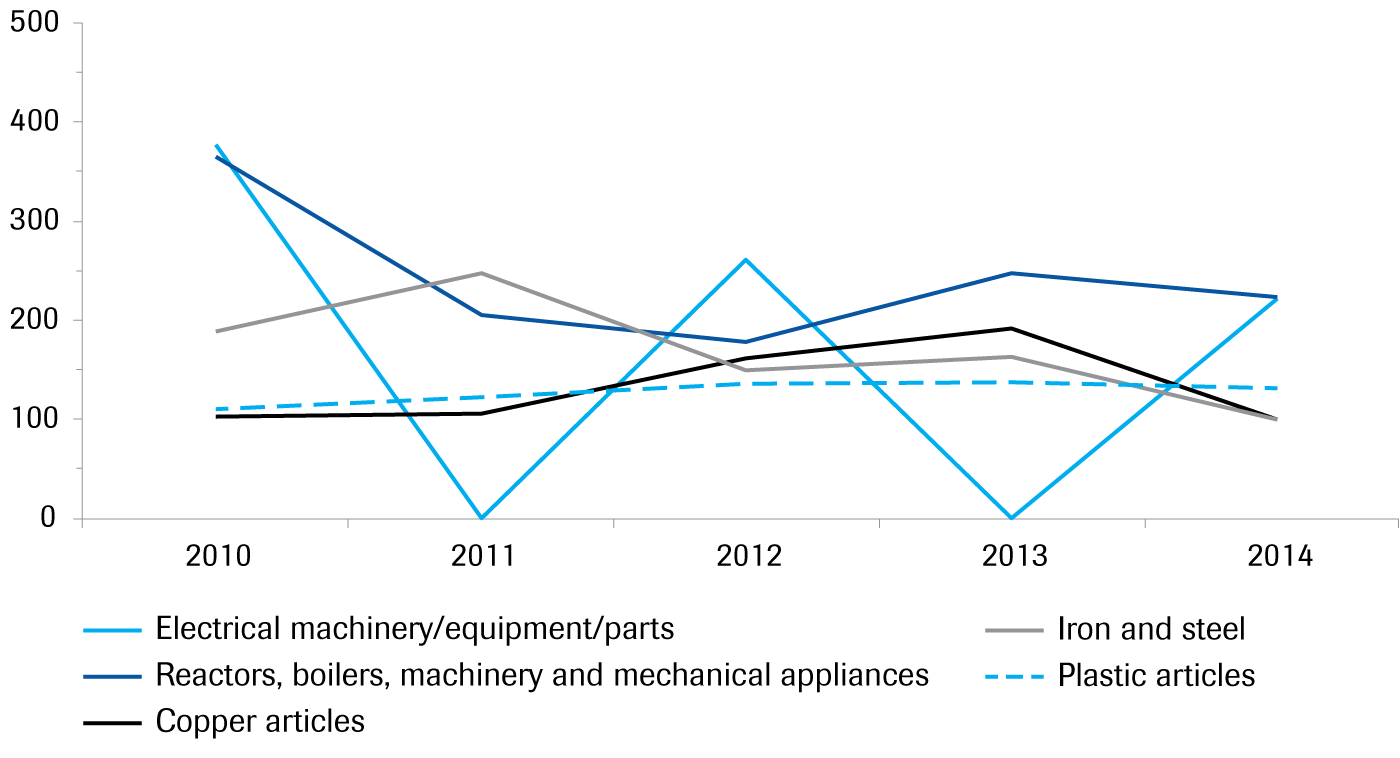

The inclusion of manufactured goods does little to change the picture described above. While it does highlight the United Arab Emirates as an important export destination, pointing at the potential impact of route closures, overall the export earnings from manufactured goods do not substantially change the pattern set by natural resources (especially the predominant metals and minerals exports to South Africa and Switzerland). Once again, a minor decline is visible in exports to Turkey, while a minor increase of exports to Syria in 2013 is maintained (see figure 7). While the export of electrical machinery fluctuates strongly over the years and a decline can be noted in the case of reactors, boilers and mechanical appliances, most other manufactured goods hold relatively stable (see figure 8). Overall, no fluctuations substantial enough to impact overall GDP growth are evident.

Export figures do not give unequivocal support to the second strand of the export argument concerning thee closure of export routes to the Gulf. The figures above show that the exports of goods to the Emirates (the only major Gulf destination for goods exports), actually increased in 2011 and 2012, before returning to 2010 levels. Exports to Turkey did show a slight decline following the outbreak of the war but rebounded and did not decline substantially until 2015.

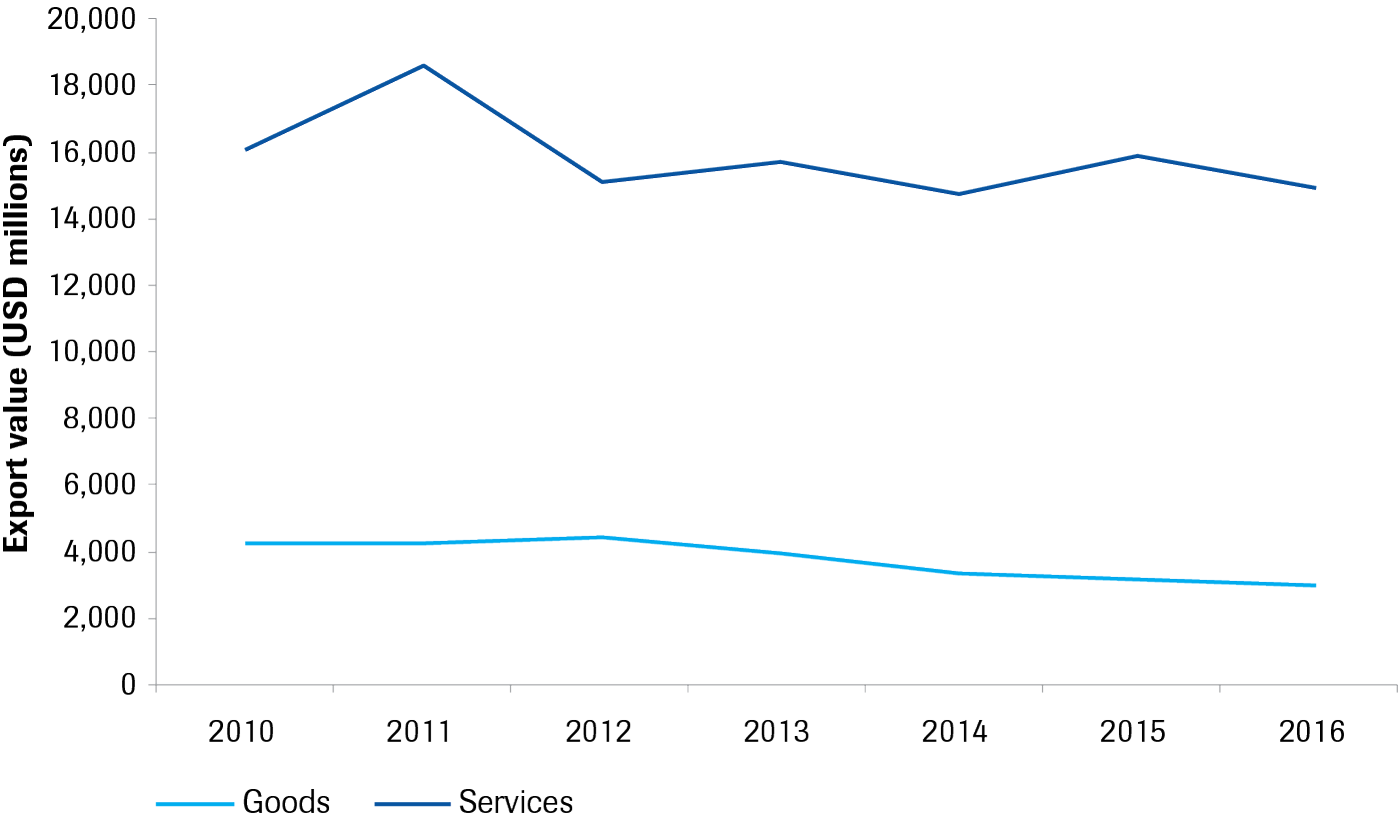

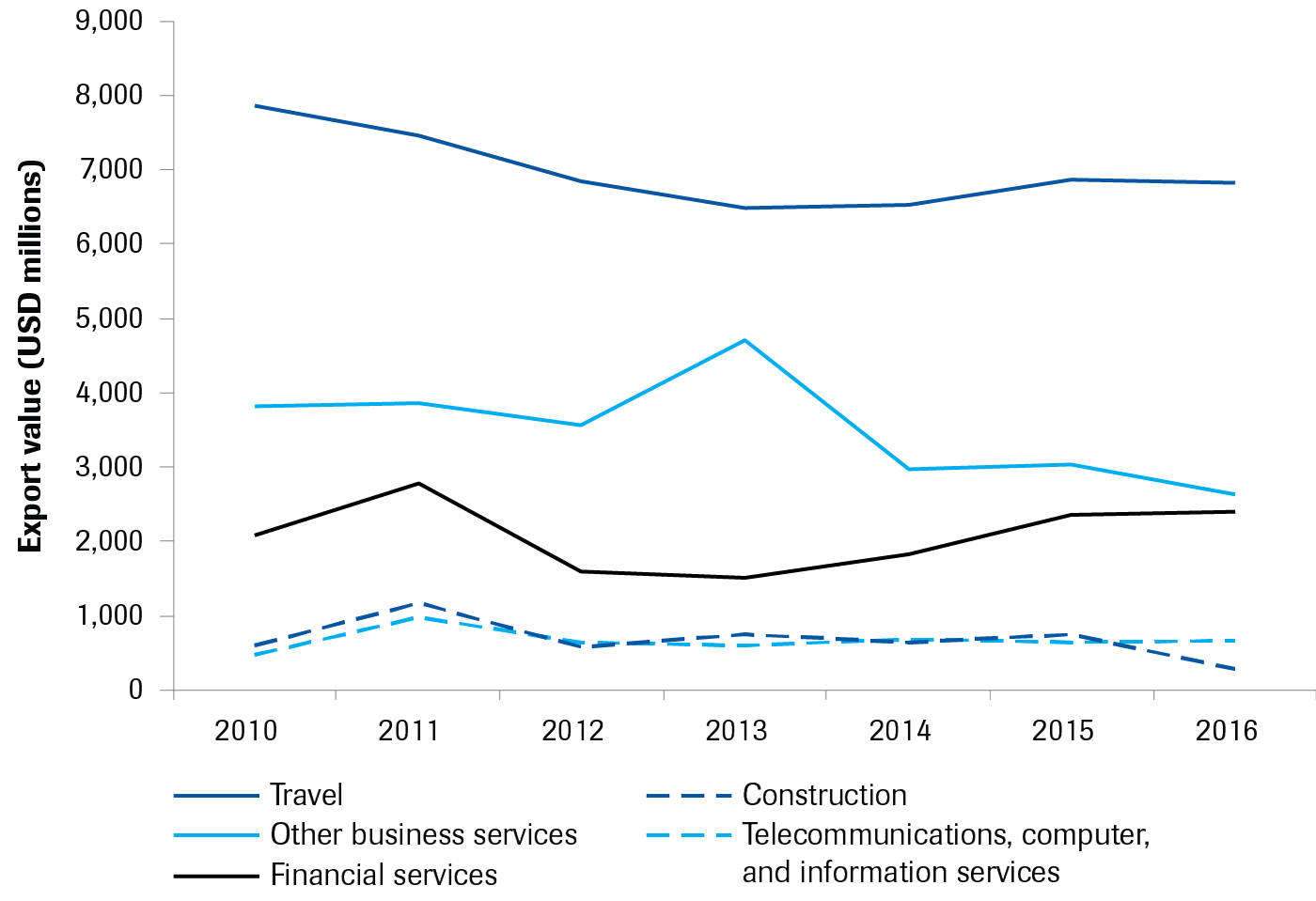

It should be noted however that Lebanese export earnings derive mainly from the export of services rather than goods, and these did decline following their peak in 2011 (see figures 9 and 10). The services exported from Lebanon consist mainly of travel related services, financial services and business services (related to various back-office functions). Of these, the travel sector in particular has suffered a significant decline owing to a drop in Gulf tourism as a consequence of frequent security-related or politically motivated negative travel advice.[42] The decline is mainly related to a levelling off of a peak in business travel in 2011, as the value of non-business travel — such as diaspora travels during the summer period — has remained relatively stable.

Earnings on financial services faced a more marked decline throughout the initial years of the war, while other business services went through a substantial uptick over the same period. Consideration should be given to how far the delivery of business services relies on the existence of direct physical land routes between trading partners. In many cases, communication facilities and flight connections may suffice. While some trade undoubtedly became more restricted because of the conflict along its main transport routes, no major exported goods or services seemed to be affected substantially enough to account for the major economic downturn Lebanon faced.

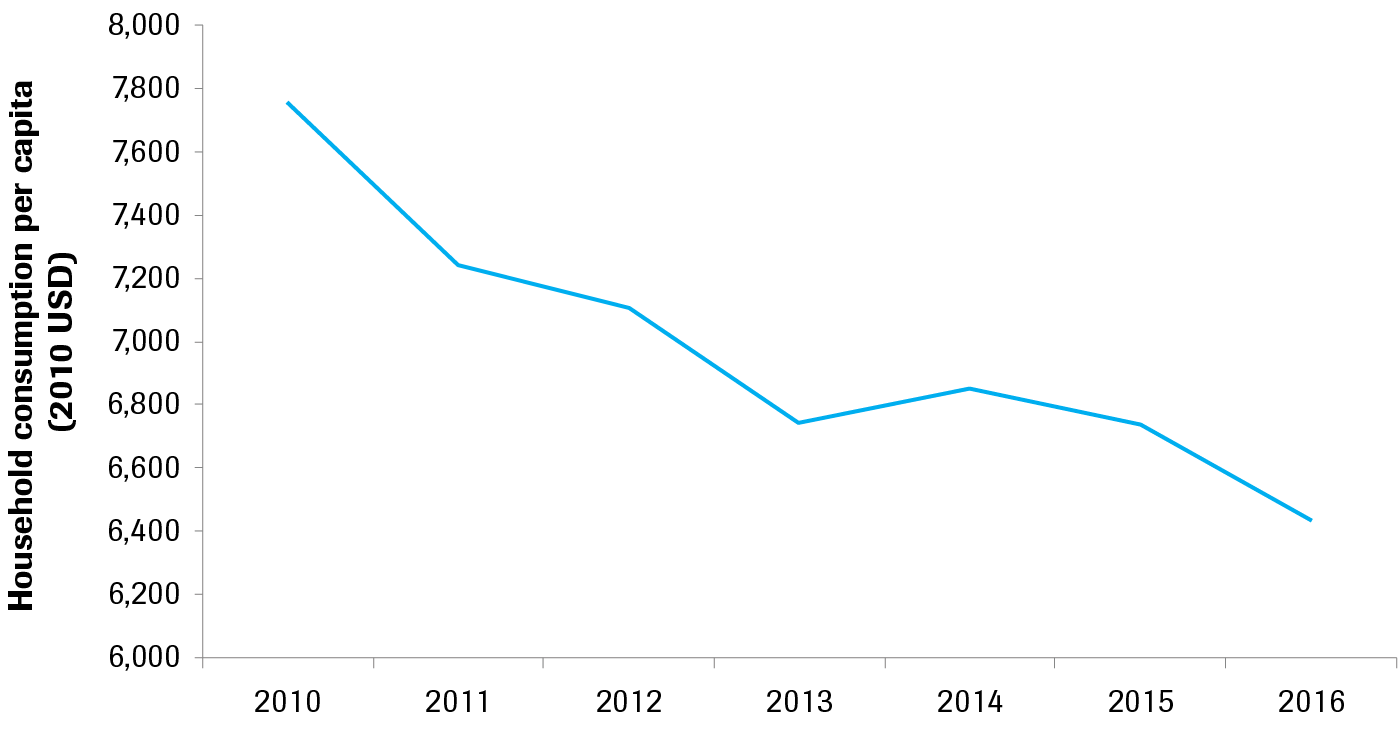

Examining the evidence potentially driving the economic downturn in Lebanon, we find that domestic factors may better explain Lebanon’s downturn than current narratives around declining exports. During this period the country was in the grip of protracted political and legislative paralysis, with Sunni and Shi’ite blocs fighting over the presidency until late 2016 and parliamentary elections seemingly indefinitely postponed.[45] Syrian war was also gradually “imported” into Lebanon’s public discourse as some political elites used the positioning towards Syrian refugees as a rallying factor among their domestic constituencies (see previous chapter). While such sectarian appeals varied in success, narratives framing refugees as an existential threat or “ticking time bombs”[46] or stressing the risk of conflict spilling over to Lebanon, may have contributed to a decline in domestic consumer spending. As the Syrian war unfolded, consumer confidence faced a relatively steep decline, hitting a low in 2013 as Syrian refugees started entering the country in more substantial numbers (see figure 11). While overall consumer spending kept growing (though at a lower rate than before), consumer spending per capita declined significantly (see figure 12) even though the substantial diaspora remittances (a considerable driver of consumer spend in Lebanon) grew over the same period.[47] In light of the importance of consumer spending to the Lebanese economy (accounting for approximately 80 to 90% of GDP), this decline may well have been a considerable driver behind the wider economic slowdown. [48]

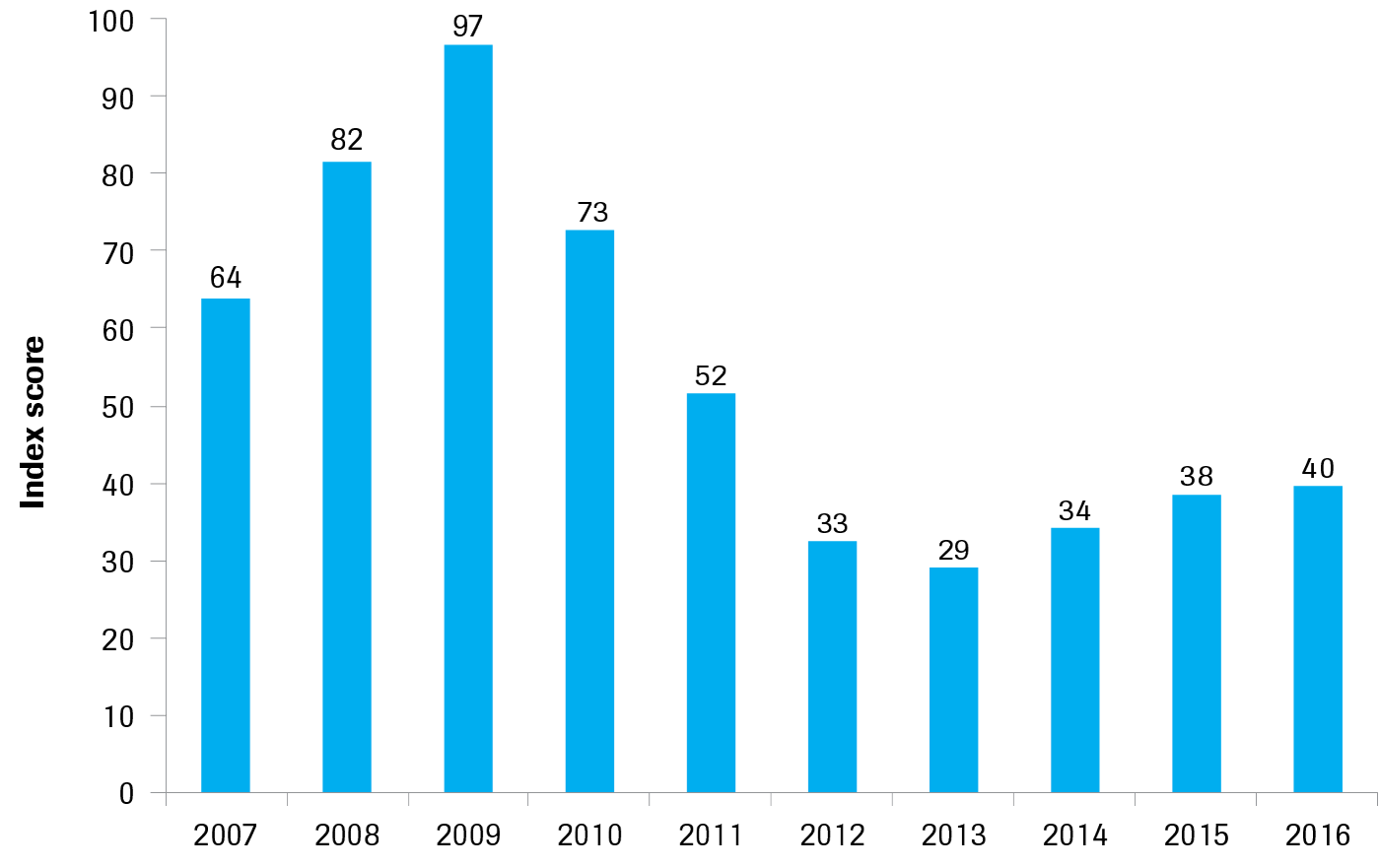

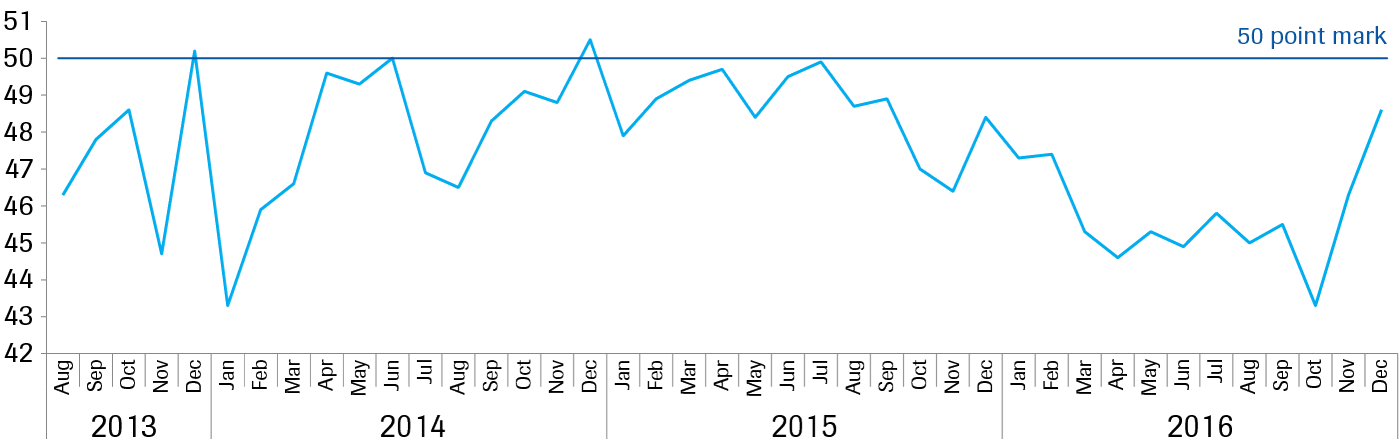

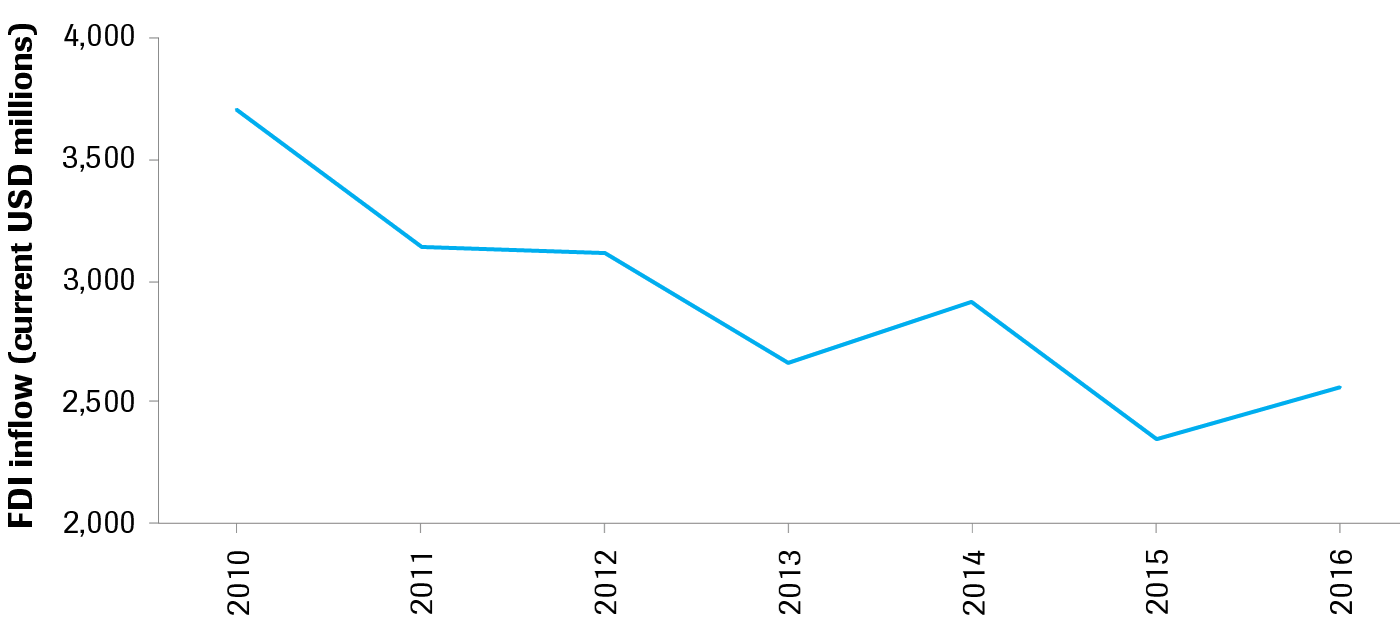

A similarly bleak picture is found in the case of corporate investments. In all likelihood responding to similar cues as consumers, capital inflows from foreign investors started to decline in 2010 and continued a downward trend throughout the Syrian war (see figure 13). Lebanon’s purchasing managers’ index has been consistently negative since 2013, only occasionally reaching the 50 point mark (indicating a neutral outlook) (see figure 14). [51] Considering the relatively inward focus of the Lebanese economy, it would seem as though the Lebanese economic prospects are mainly related to perceptions and expectations of domestic risk factors, rather than driven by export opportunities. The decline in corporate investments appears to be related to the broader sense of insecurity, fuelled by the way events in Syria are framed in domestic political narratives, rather than any direct impact stemming from the crisis.

2.2 Effects of the refugee influx

While the aggregate macro-economic view may highlight the wider drivers of Lebanon’s economic developments, it does not account for the highly unequal impact of the refugee influx on individuals in Lebanon’s diverse and complex society with high income inequalities and complex redistributive system. Following the onset of the Syrian war, the influx of Syrian refugees has visibly affected the lives of the vast majority of Lebanese citizens, whether through their joint use of public spaces or consumption of the same basic goods and services. Over a million Lebanese citizens that were already near or below the poverty line have been feeling the pressure.[54]

On a political level, the refugee presence is reflected in narratives concerning Lebanese hospitality, as well as in narratives of Lebanese victimhood in the face of growing population pressures.

The narrative of Lebanese victimhood from mass displacement in based on two claims:

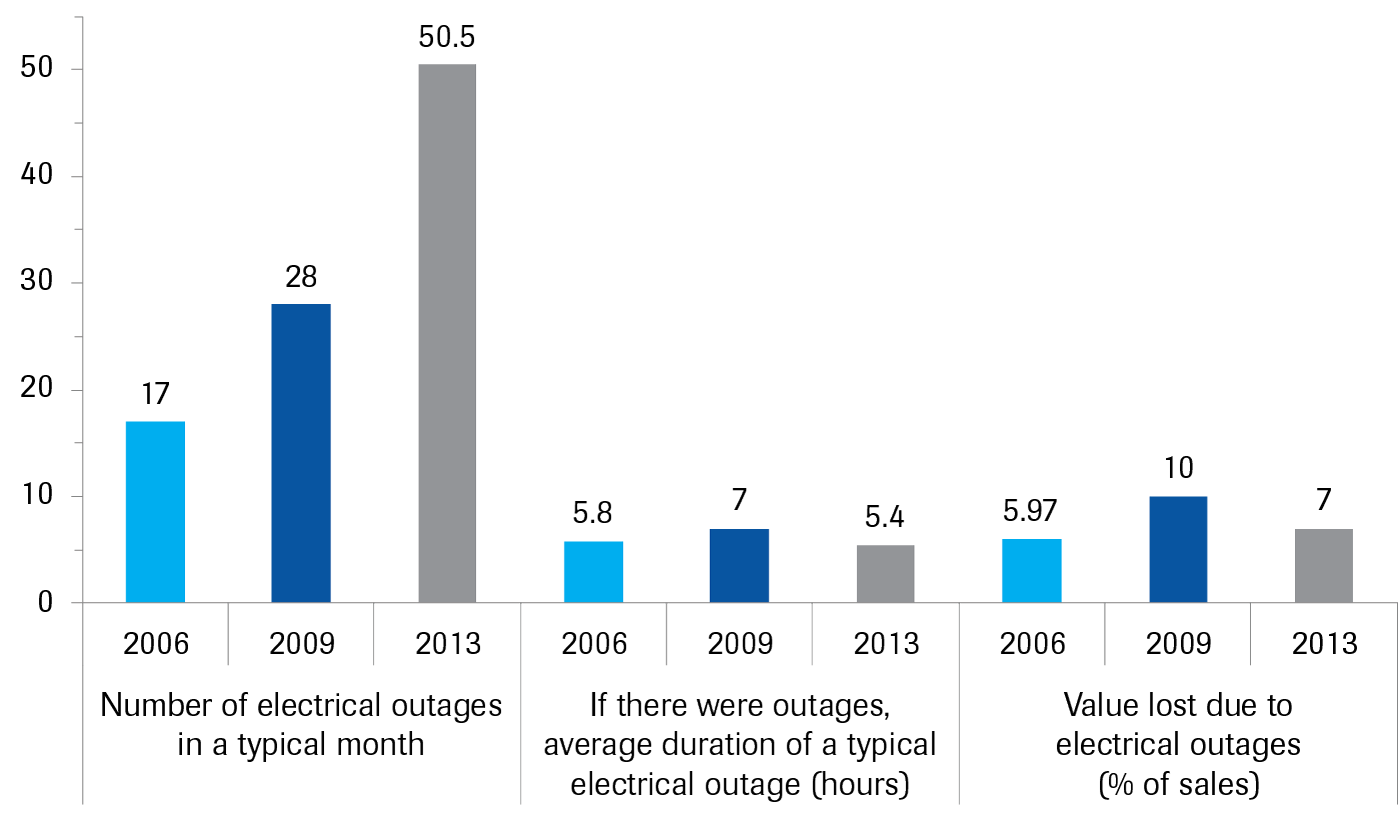

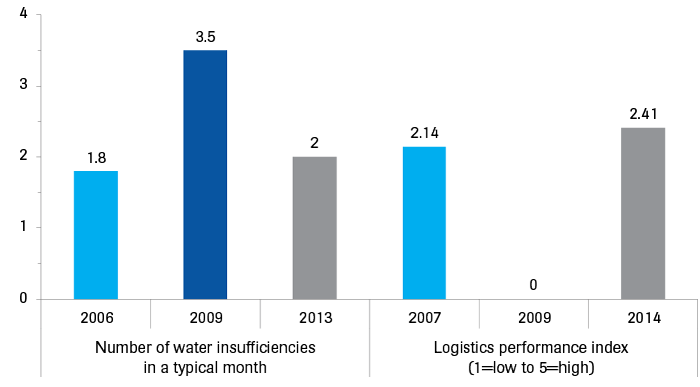

Firstly, it stresses the heavy strain on Lebanese public services and infrastructure. The additional strain put on utilities, waste disposal and roads by the presence of over a million refugees is indeed substantial, and in all probability does cause a tangible decline in service levels. The resulting failure of basic services is highly visible in daily life — seen, for instance, in the 2015 garbage crisis — and provides an easy rallying point for anti-refugee sentiment. It should be noted, however, that the system was not able to handle the demand put on it before the influx of Syrian refugees. While services such as electricity provision have declined, most Lebanese households have been relying on alternative solutions such as electricity generators for years.[55] The Lebanese state is not focused on the public provision of such goods and services but has instead allowed the existence of informal private markets to cater to these needs. These private markets are often inaccessible to those on low incomes, who are forced to rely on threadbare public utilities. The increased strain on the public system has highlighted and allowed for the politicisation of pre-existing failures rather than causing them (see figure 15a and 15b).

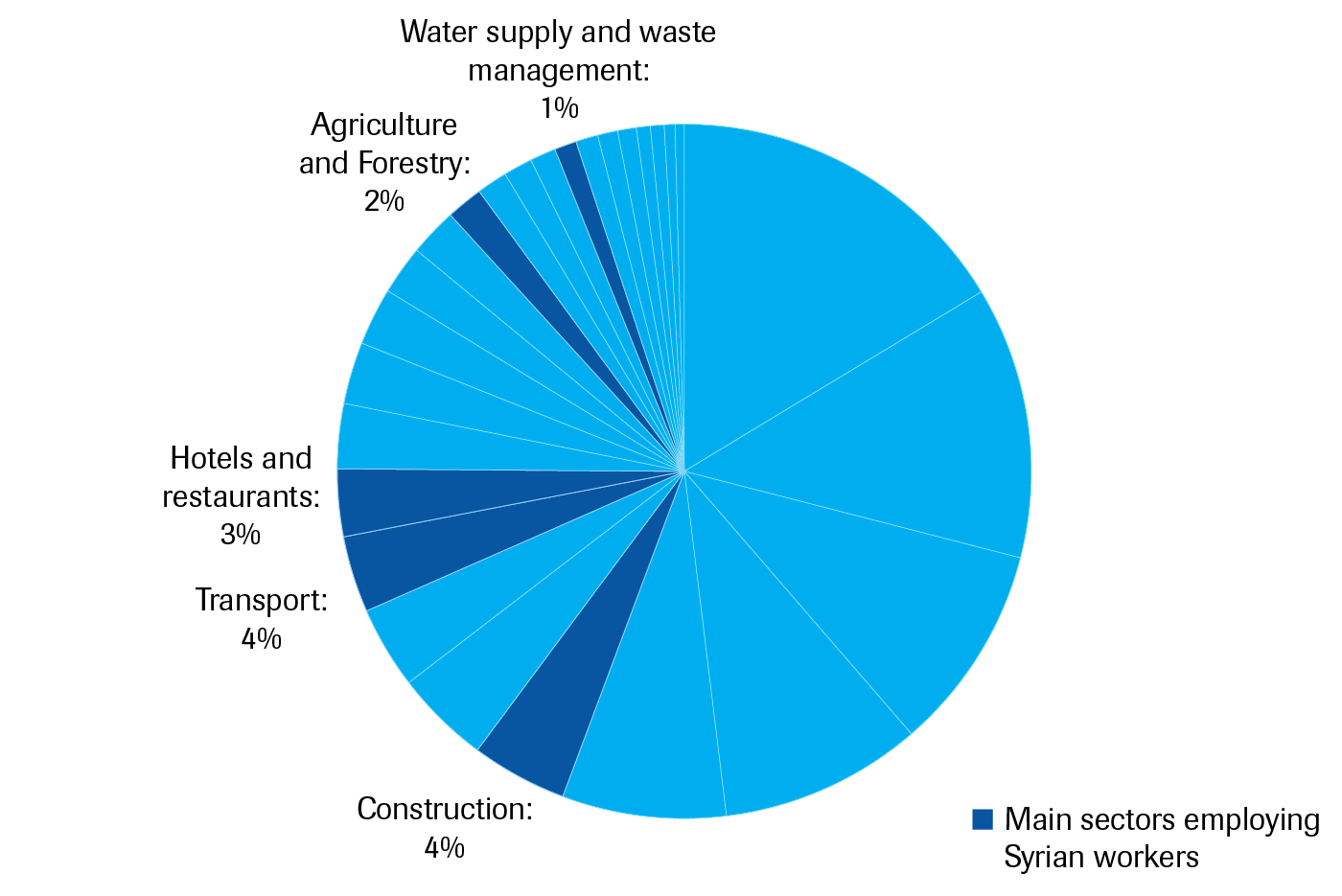

The second strand of the Lebanese victimhood narrative surrounds increases in the already high unemployment rate due to competition between Syrian refugees and Lebanese. Overall unemployment is indeed substantial in Lebanon (6.3 %)[58], and even higher among young people (16.5 %).[59] Yet patterns of job competition are more complex than this narrative suggests. While competition between Syrian refugees and Lebanese is significant and highly visible in the transport sector (e.g. taxi drivers) and restaurant services, the significance of these sectors in the Lebanese economy is limited (see figure 16). In practice, most Syrian refugees work informally in the construction and agricultural sectors, which were already heavily reliant on migrant workers (often, indeed, from Syria). While job competition is strong in these sectors (and may negatively affect wages), it mainly takes place between migrant workers from different countries and among Syrian refugees themselves, rather than involving Lebanese labourers. An example can be seen in the construction sector. A Syrian migrant labourer in the informal construction sector can earn a wage of approximately 15.000 LBP (10 USD) for an 8-12 hour day.[60] Given this wage, his monthly income is likely to end up around 200 USD/month or lower (assuming 20 days of work a month). Such an income puts a Syrian worker at the bottom end of the labour market.[61]

While labour competition between refugees and migrant workers may be a worrying factor from a humanitarian point of view, it should be noted that the Lebanese economy has long relied on the cheap foreign labourers. Syrian workers have long fulfilled this role.[63] A number of small and medium sized enterprises, including some based in the regions absorbing the most refugees, actually cited the influx of refugees as a key factor in their ability to overcome constraints imposed by Lebanon’s poor infrastructure and regain some competitiveness. As a number of interviewees noted, the main driver behind the employment of Syrian refugees has been their willingness to work longer hours at lower wages than other migrant workers, not their cultural proximity or shared language.[64] The arrival of Syrian refugees allowed these firms to produce at competitive prices, regardless of the otherwise high operating costs in Lebanon. While many businessmen expressed their preference of employing Syrian workers, a number also noted that they did not employ Syrians in consumer-facing positions as their employment is highly politicised and may cause a backlash against the business.

In addition to cost savings on their operations, a number of businesses also benefited from additional demand. While the influx of additional loans and grants into Lebanon to fund the refugee response provides an obvious stimulus, the additional demand for basic goods by refugees (estimated at USD 1.6-1.8 billion for 2017) [65] and the impact of an influx of aid workers should not be ignored.

Effectively Lebanon’s “personal status system thus serves to deny the Lebanese their inalienable rights as citizens, and obliges them to be members of a recognised sect and hence sectarian subjects”, [66] instead of citizens. The political system is not designed around the provision of public goods, but around the clientelistic allocation of goods through sectarian elites to their own constituencies. The effects of the Syrian crisis have been filtered by the same sectarian clientelistic systems, thus impacting Lebanon’s various communities in different ways. The lack of clear public data on the impact and the wide array of interpretations/narratives explaining the impact reflects the particularistic power relations that structure Lebanon’s political and economic space.

The macro-economic overview presented in this chapter sheds a light on the overall impact of the Syrian crisis, but cannot give a comprehensive overview of the sectarian differences that are feeding the political discourse. A prime example of these differing sectarian interests was illustrated in an interview with a high-ranking political appointee at the Lebanese Ministry of Labour. Stressing the impact of the reduced export opportunities to Syria, this advisor suggested the Syrian refugees could stay if the EU would guarantee increased agricultural imports from Lebanon. In the context of the wider response, the value the these additional imports would have been negligible compared to the Lebanon-wide refugee response, and it does not stand in relation to any significant losses due to exports to Syria. The offer then should be interpreted from a sectarian rather than a public point of view, as the influx of low wage Syrian labour coupled with additional EU demand would provide a major benefit to this interviewee’s predominantly agricultural constituency.

Besides inter-sectarian differences, notable intra-sectarian class inequalities also exist. The effectiveness the clientelistic allocation of basic public goods relies significantly on Lebanon’s high income inequality.[67] While the costs associated with the Syrian crisis may to a considerable degree be offset by new economic opportunities, it should be clear that while the costs affect all Lebanese (and low income Lebanese in particular), the opportunities are only accessible to a select few. Whereas a medium sized company may benefit from reduced labour costs and face only minor increases in the costs of operating its electricity generator, a low income Lebanese employee may not be able afford private electricity provision nor hiring any kind of employee. The benefits of the Syrian crisis are thus likely to accrue to the Lebanese elite, while the costs hit lower income Lebanese population disproportionally hard. Though this pattern of inequality predates the onset of the Syrian crisis, it has been aggravated by the influx of refugees. As a result, the issue has become a tool for political mobilisation.

The sectarian system has proven hard to navigate for donors seeking to support refugee and host communities through humanitarian and development efforts. Donors departing from a Western narrative that emphasises the central role of the state risk getting trapped in Lebanon’s sectarian maze. As a consequence, donors who seek to partner with the central Lebanese government to provide public goods without sectarian targeting are unlikely to achieve tangible results.