Introduction

Due to the openness of the European economy, free and open trade is crucial for the European Union (EU).[1] Trade will remain an important engine of economic growth in the future. In view of the expectation that 90% of global economic growth will be generated outside the EU in the next 10 to 15 years, it is extremely important for Europe that global trade is not restricted.[2] As the EU states in its trade strategy: ‘With most world growth expected to take place outside the EU in the near future, trade and investment will increasingly underpin our prosperity: a prosperous Union hinges on a strong internal market and an open international economic system. We have an interest in fair and open markets, in shaping global economic and environmental rules, and in sustainable access to the global commons through open sea, land, air and space routes’.[3]

Europe holds an exceptionally strong position in the field of international trade. The EU is the world’s largest exporter and importer of goods and services, the main investor in direct foreign investments and the main recipient of foreign investments. It is the main trading partner of some 80 countries and the second largest trading partner of another 40.[4] This makes the EU the biggest trading block in the world, accounting for about 15% of world trade in goods and 22.5% of world trade in services.[5]

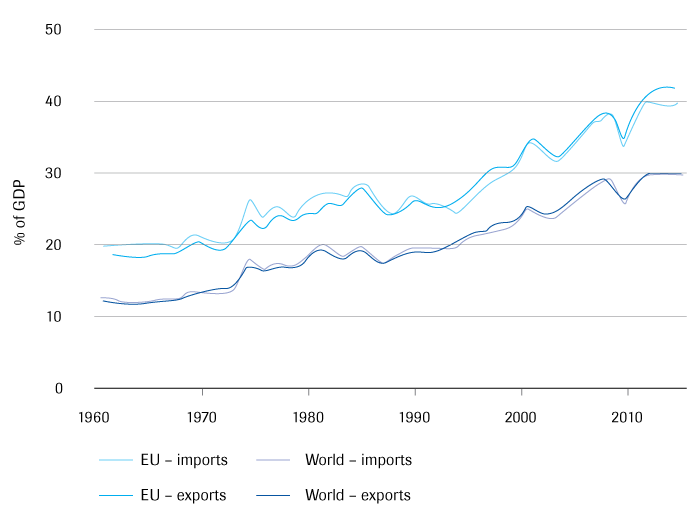

The main indicators for the importance of international trade for the European economy are the export and import ratios. These ratios show the share of exports and imports in the economic growth. The higher these ratios, the greater the international interdependence of the economy. Figure 1 shows that these ratios for Europe lie at 42% and 39% of gross domestic product (GDP) respectively. This shows that the European economy is even more interdependent than the global average, for which the ratios lie at around 30%.

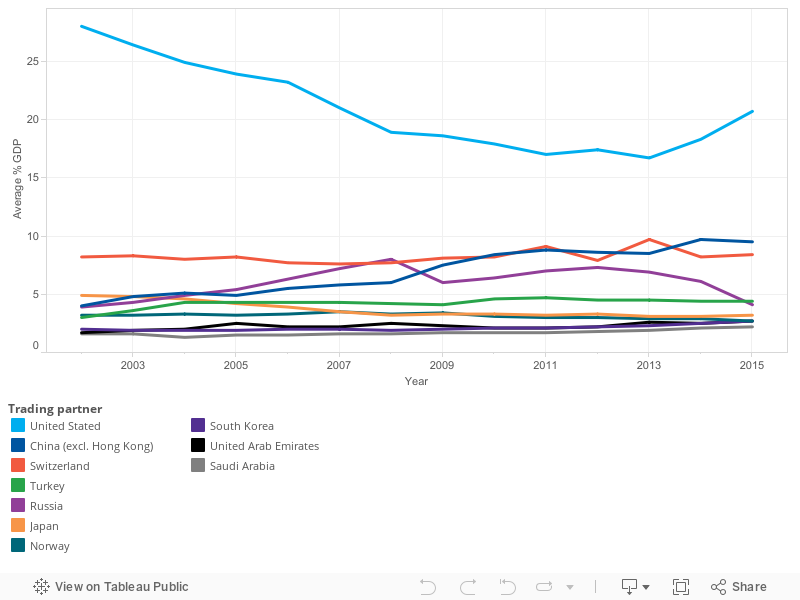

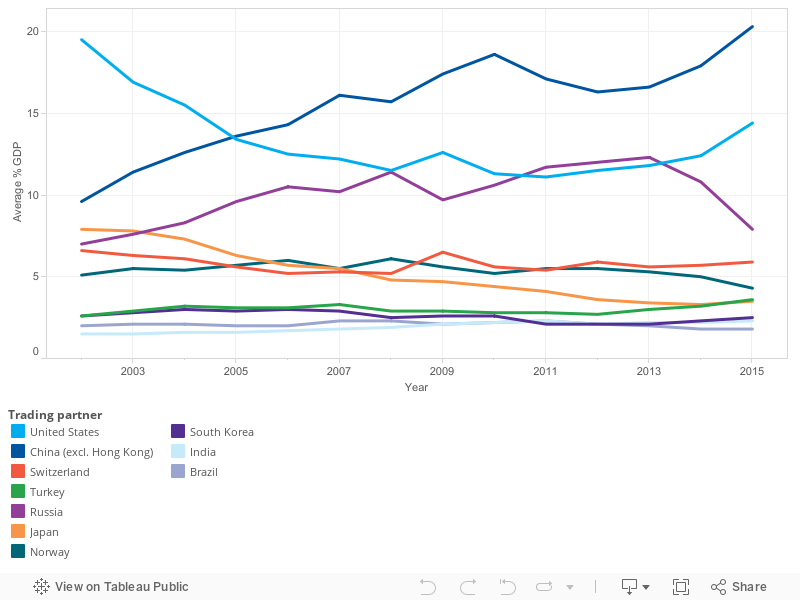

The US is still the main export region for the EU, with a share of about 20% in EU exports. The US is followed at a substantial distance by China, but the Chinese share has more than doubled since 2002 and reached more than 10% in 2015. The rise of China in European imports is particularly impressive. About 20% of all European imports come from China, compared with an American import share of 14%. China has consequently become the second most important trading partner of the EU in the past 15 years (see Figures A and B in the pop-out window).

Threat assessment

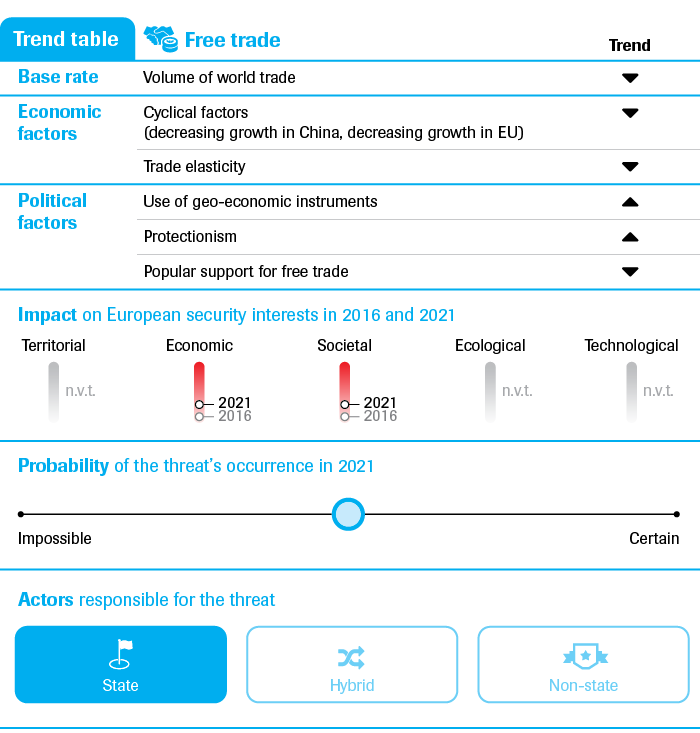

Although the EU has a strong position in the field of international trade, it is important to realise that the growth in world trade is under pressure. A trend analysis that identifies the main threats to international trade is presented below (see also Table 1).

The base rate

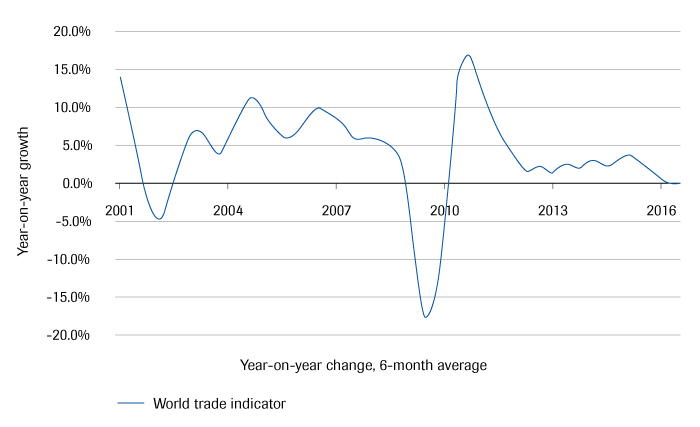

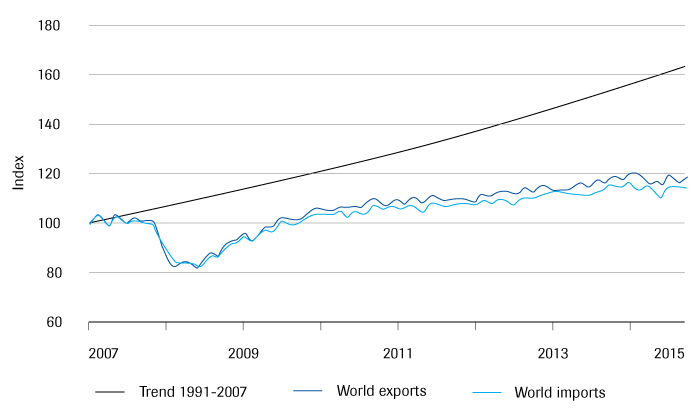

The financial crisis of 2007-2008 was followed by the Global Trade Collapse of 2008-2009. There was then a brief recovery, after which the growth in world trade fell back again to a structurally lower level. Figure 2 shows that since 2008, world trade growth has fallen below the trend growth of 1991-2007 and has not been able to recover.[7] The world trade monitor of the Netherlands Bureau for Economic Policy Analysis (CPB) shows the same (see Figure C). This indicator shows that growth in world trade even came to a standstill in 2016.

Determining factors

A number of reasons can be given for the diminishing world trade growth. A distinction can be made here between economic and political factors (see also Table 1). With regard to the economic developments, in the first place cyclical factors such as slowing economic growth in China, the slow recovery in Europe and the additional falling demand for commodities led to lower trade growth. The transformation of the Chinese economy from an export-driven economy to an economy focusing more on domestic consumption has major consequences for world trade growth.[9] Precisely because of the increased importance of China in European exports, and particularly also in imports, this development affects the economic position of the EU.

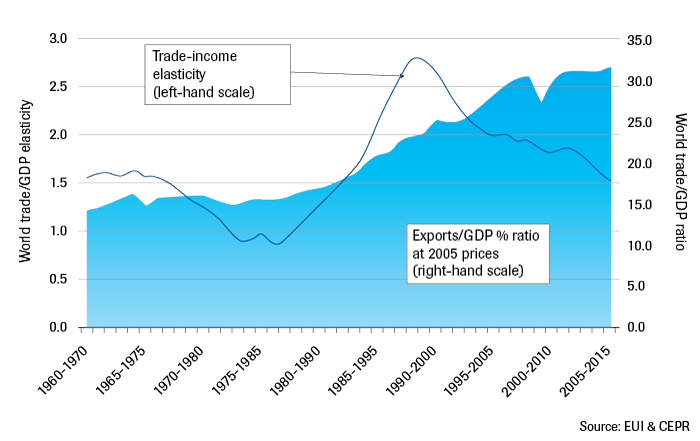

In addition, there is an important structural economic explanation for the slowing world trade growth. Here the changing relationship between global trade and economic growth, the ‘trade elasticity’ is considered. In recent decades the general rule was that world trade grew twice as fast as global GDP, but this is no longer the case.[10] The rapid growth in world trade in the 1990s was primarily the result of technological innovations. These led to sharp reductions in transportation, communication and transaction costs and it became possible for companies to cut up production processes efficiently and to spread production optimally over more countries on the basis of specialisation. As a result, value chains developed, in which the different parts of a product were produced in different countries.[11] This process automatically let to growing trade between countries, particularly intra-firm and inter-firm trade, as a result of which trade elasticity increased. However, there is a physical limit to the extent a product can be fragmented any further.[12]. As a result, the contribution of value chains to international trade is falling. The appeal of value chains is also diminishing as a result of increasing costs in the countries to which production processes have been transferred. Consequently, it has become attractive to shorten supply chains again, or to re-shore them.[13] In the coming years, trade elasticity will remain lower than in the 1990-2007 period. Exports will also become a less important driver of economic growth, because important countries such as China will be focusing more on the domestic economy.[14]

Declinging trade elasticity

The ratio of world GDP and world trade growth is known as ‘trade elasticity’. The Figure below shows that trade elasticity reached a peak of almost 3 in the 1990s and early years of this century. This means that with world GDP growth of 3%, world trade was growing by 9% at the time. The elasticity trend then fell and has recently even dropped below 1.

Two matters are given as the main reasons for the diminishing trade elasticity. Firstly, the reintegration of China and Eastern Europe into the world economy appears to be levelling off. The Chinese transformation into a consumer-driven economy plays a particularly important role in this. In addition, the intensity of fragmentation of the value chain is slowing down: there is a physical limit on how much a product can be fragmented any further.

In addition to these economic developments, world trade growth is threatened by a number of political factors. A distinction is made here between the deployment of geo-economic instruments and protectionist measures. It is not always simple to separate these, but the former primarily concerns the deployment of economic instruments or policy to support the strategic foreign policy of a country (and is therefore primarily politically inspired), while economic considerations predominate in the deployment of protectionist measures.

With regard to the deployment of geo-economic instruments for foreign policy, there is a wide range of possibilities. Examples include financial and economic sanctions, calling for public boycotts, a full economic blockade, increasing import inspections, gas and oil boycotts, exclusive clubs of countries that form a trading bloc, etc. In an increasingly interdependent global economy, the deployment of these instruments has become increasingly effective. Important examples are the deployment of European and American sanctions against Russia following the Russian annexation of the Crimea and Western trade restrictions against countries such as Iran, Venezuela and Myanmar. While in the past, such sanctions affected the entire population, today efforts are being made to make such sanctions smarter: they are directed at particular individuals or companies. Geo-economic measures harm international trade through the direct restriction of trading possibilities, growing uncertainty and the deteriorating investment climate. However, according to the World Economic Forum, among others, geo-economic instruments will be used more frequently in the coming years, because of their effectiveness.[15]

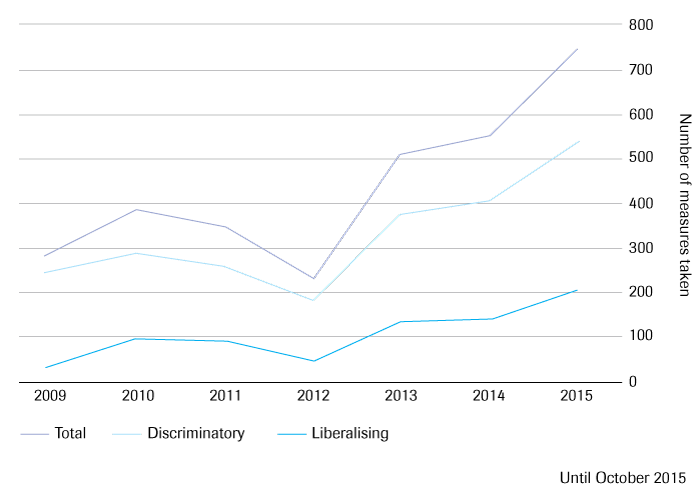

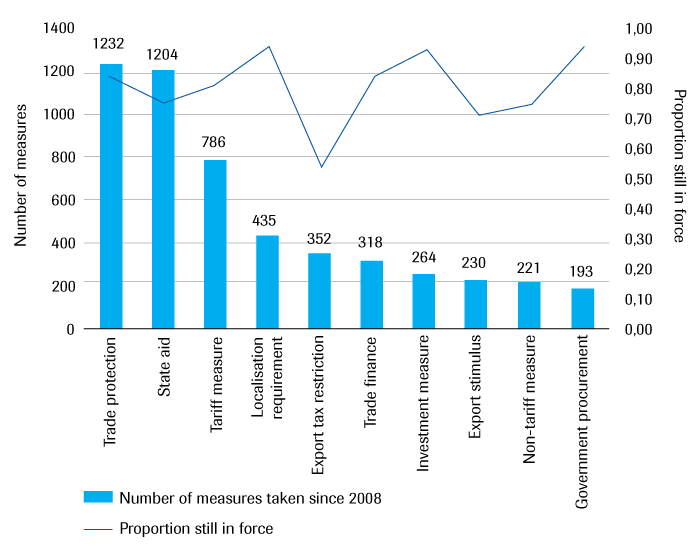

Another important development in the political sphere is the growing protectionism. Figure 3 shows that the number of trade-restricting measures has been rising sharply since 2012. However, this growing protectionism is reflected less and less often in direct instruments with import-restricting effects such as higher import duties, import quotas and competitive devaluations. The only direct import-restricting measures that are still deployed relate to the protection of the domestic economy against dumping and subsidised imports. Instead, governments are turning increasingly to indirect instruments that are less transparent and attract less attention, such as state aid in the form of subsidies, government procurement, non-transparent trade financing and regulation relating to local requirements, such as mandatory employment of local workers, mandatory use of local product components and mandatory local storage of data. Such instruments lead to a non-level playing field between countries.

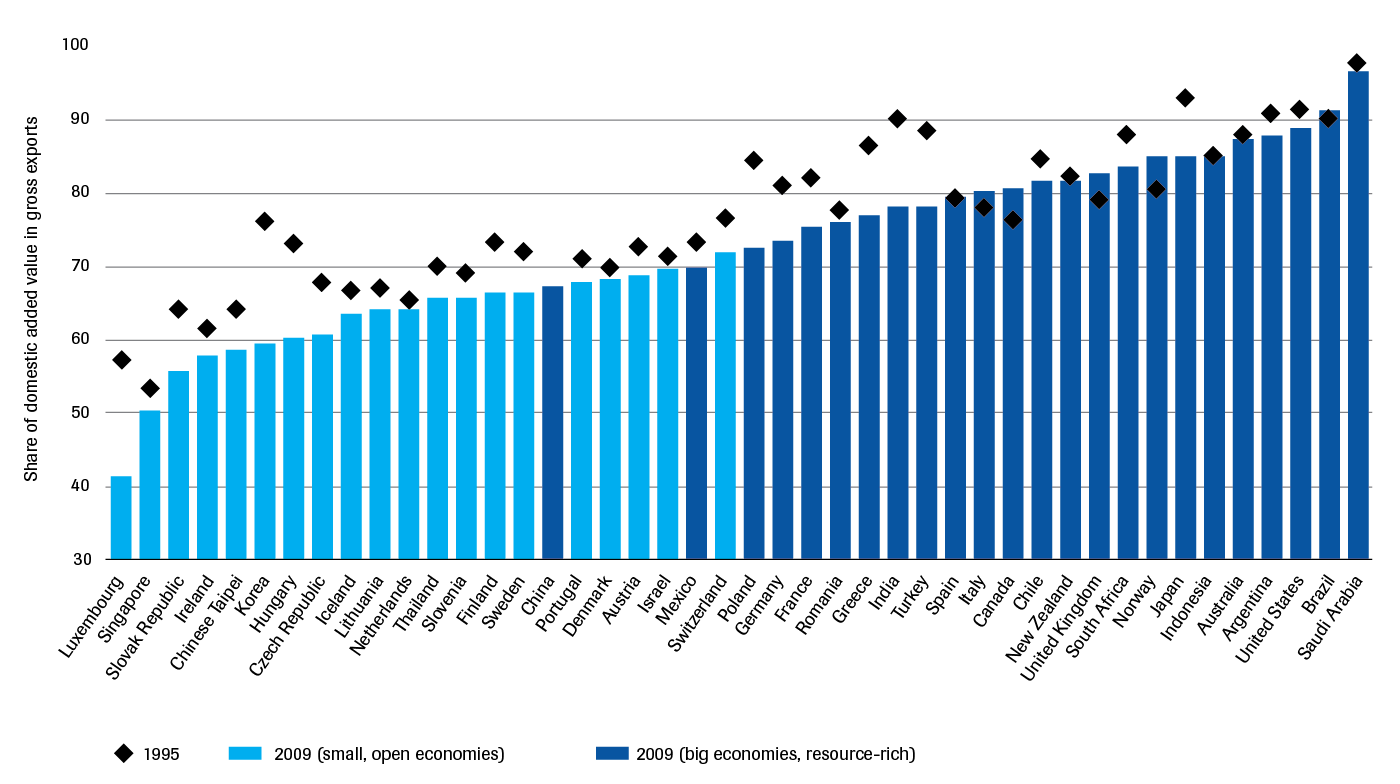

Apart from the fact that import-restricting measures are less attractive because they are immediately noticeable, an economic argument also plays a role. The aforementioned rise of value chains and the growing interdependence of economies mean that export products increasingly consist of parts that have to be imported from other countries.[17] Figure D shows that the share of domestic added value in gross exports fell in the 1995 – 2011 period. As a result, making import products more expensive is ultimately detrimental to a country’s own export products. If China, for example, increases import duties on car engines, then the ultimate Chinese export price of those cars will also rise. In short, import restrictions harm the competitive position of a country’s own exports. Figure 4 presents this development.

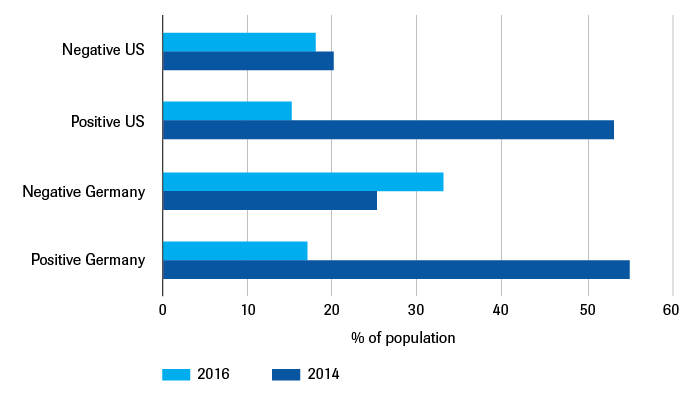

In addition to the growing use of the abovementioned trade-restricting measures, popular support for growing economic integration appears to be shrinking. The World Trade Organization (WTO) already identified this trend some years ago.[19] Opinion polls also support this claim. A large survey conducted by the Pew Research Center in 2014, in which 44 countries participated, showed that populations generally take a positive view of international trade: 81% of the respondents regarded international trade as positive. However, precisely in the developed economies, a more sceptical attitude is emerging. The respondents have less confidence in the other effects of trade on, for example, wages and employment.[20] Free trade agreements are also under (severe) pressure; this is illustrated by the rapidly diminishing positive view of the Transatlantic Trade and Investment Partnership (TTIP) in the US and Germany (see Figure 5). Even clearer was the signal given by US president-elect Donald Trump, who announced that on the first day of his presidency he would scrap the Trans-Pacific Partnership (TPP). This free trade agreement was to further liberalise the trading of 12 countries around the Pacific (including the US, Japan and Canada, but without China). Falling support for free trade agreements was also visible in the closing phase of the negotiations on the Comprehensive Economic and Trade Agreement (CETA), a free trade agreement between Canada and the EU, in which Wallonia put its foot on the brakes over fears of unfair competition and dissatisfaction with an arbitration regulation.

Impact and shocks

For Europe, developments in world trade are of major importance. World trade growth is under pressure and will remain so in the coming years. However, the chances that economic and political factors will have such an impact on world trade growth that they damage the foundations of an open, efficient and effective economy are not seen as very probable. The self-regulating character of the market means that economic developments have a less permanent effect. The risk lies more in the aforementioned political factors, particularly in the growing protectionism and falling popular support for free trade. If these two factors take on serious dimensions, they will harm the openness and thereby, the foundations of the European economy. Much of the threat comes from states that deploy protectionist measures and geo-political instruments, but also from non-state actors that drive the debate on the importance of free trade (such as popular movements).

Are sudden developments that could change this assessment conceivable? This question was put to experts in the Clingendael Expert Survey (see Figure E). The experts stated that a meltdown of the global financial system, for example, would have a large to very large impact, but the risk of this happening was regarded as unlikely. Should such a meltdown nevertheless occur, it would have serious consequences for world trade growth, similar to or even worse than the financial crisis of 2008, which spread from the financial markets to the real economy. The rise to power of European politicians who oppose free trade and deploy more protectionist measures is also regarded as a threatening development.

Shock

Free trade regime

Actors and institutions

The international trade system consists of a complex set of organisations and institutions in which governments agree international, regional and bilateral treaties and conventions. Both the number of organisations in the field of trade and the organisations themselves continue to grow gradually.[22] World-wide, the WTO is the most important multilateral organisation in the field of trade, and since its formation has played an important role in the development of a global rules-based international trade regime. Other important players in this field are the Organization for Economic Co-operation and Development (OECD) and the United Nations Conference on Trade and Development (UNCTAD). The biggest economies meet regularly in informal settings within the G7/8, or together with the main emerging economies through the G20. At the regional level, the various free trade zones such as the EU, the African Union, the North American Free Trade Agreement (NAFTA), the South American Mercosur and the Association of Southeast Asian Nations (ASEAN) are the determining alliances in the field of trade.

Norms and rules

The trade system is based on a number of norms and rules (see Table 2). The main overall norm concerns the importance of open and non-discriminatory trade on the basis of reciprocity. The predominant idea here is that trade is promoted by liberal trade policies in which trade is restricted as little as possible by government intervention. Another important norm is that in principle, any trade disputes between (groups of) countries will be solved in a multilateral setting, i.e. within the WTO. The WTO covers a broad package of rules on matters including trade in goods and services and intellectual property. It has also laid down a number of important principles that form the basis of the multilateral trade system. These are the principles of non-discrimination, reciprocity of concessions, binding and enforceable commitments and transparency. Unfair practices such as export subsidies, import duties and dumping are not permitted. There are exceptions to these basic principles: for example, developing countries may be favoured and parties may waive their mutual trade restrictions on a preferential basis in the interests of economic integration, for example in order to form a free trade zone.

|

Norms |

Rules |

|---|---|

|

Importance of open and non-discriminatory trade |

Non-discrimination |

|

Liberal trading policy |

Reciprocity of concessions |

|

Trade disputes resolved within the framework of the WTO |

Transparency |

|

Broad package of WTO rules on trade in goods and services and intellectual property. |

The credibility of the WTO as a negotiating forum has suffered considerably in the past decade, because multilateral negotiations on a new world trade agreement (the ‘Doha round’) has progressed only with great difficulty for many years. This is partly due to the fact that the ‘low-hanging fruits’ (i.e. the less controversial questions such as rates) have already been plucked. The questions currently on the table (such as services, intellectual property, etc.) are considerably more complex. At the same time, global talks on world trade have become increasingly complex as a result of shifting power relationships. The Doha round reveals major differences between the positions of industrialised nations and that of the main emerging nations. The biggest bottlenecks include the resistance of the emerging nations (China, India, Brazil) to the desire of the US for greater access to their markets. Secondly, there is the food security issue: emerging nations, particularly India, want it to be possible for them to build up food stocks. In order to break through the impasse, at a certain point countries started negotiating on less controversial elements. In that regard, agreement was reached at the ministerial meeting in Bali in 2013 on a trade facilitation agreement. Two years later in Nairobi, progress was made by reaching agreements on the rapid phase-out of the agricultural subsidies. Nevertheless, (by a long way) this did not bring a new trade agreement into view. In order to make progress in certain areas, groups of countries increasingly negotiate within the WTO framework on sector-specific agreements, such as those in the field of information technology or financial services. These plurilateral treaties bind only a limited group of WTO members, but they were drawn up in accordance with WTO norms and are explicitly intended to allow more members to accede to them at a later date.

Despite the difficult multilateral negotiations, there is broad agreement among the member states on the free trade norm of the world trade system. Most of the countries also comply with the trade rules already agreed. For example, the promise to pursue free trade is regularly included in the closing declarations of the G20.

Compliance

Although most member states comply with the trade rules set, a substantial increase has been visible for years in the deployment of protectionist measures, the biggest offenders being the US, Russia and India. In view of the size of its market, the spotlight is also falling increasingly on Chinese trade policy. The country is accused of protectionist measures, such as illegal subsidies and closing off (parts of) markets from foreign investors. Although the G20 state time and again that they wish to ban protectionism, this seems no more than lip service. For example, the WTO has noted a significant increase in trade-restricting measures among the G20 members.[23]

Another discussion is less about compliance with the rules as about a different view of the structuring of the economy. During the financial crisis of 2008 in particular, it became clear that the market capitalist model also had its shortcomings. The Chinese state capitalist model, distinguished by strong government intervention, became an attractive alternative for developing countries, particularly in view of the strong economic growth that China is (or was) undergoing. China is not aiming to replace one model with the other, but to win acceptance at a global level that there is no need for a universal economic model. Nevertheless, the fact that China (and other emerging markets) aim for free trade, but with different ideas about government intervention, places the system as we known it under pressure. An underlying problem is the lack of liberalisation of Chinese politics.

Apart from the question of whether there is compliance with the existing rules, it is important to be aware that new rules are now not only drawn up in a multilateral framework, but above all, in a regional or bilateral setting. The lack of progress in the multilateral Doha round has led many countries to start negotiations on bilateral or regional trade agreements as an alternative for further global liberalisation of world trade: including the European Union. Although the European Commission states that the multilateral system will remain the cornerstone of EU trade policy, the Union also has an ambitious bilateral agenda. This ambition applies both for the number of countries with which the EU has contracted or wishes to contract free trade agreements and for the content of the agreements, which cover many subjects (sustainable development, goods and services, investments, etc.).[24] One example is the aforementioned TTIP (which, however, is under serious pressure with the election of Trump as president), but the EU is also negotiating on free trade agreements with Japan, South Korea, Peru and Australia. At the end of 2014, the EU concluded an agreement with Canada on a free trade agreement (CETA); that agreement was finally signed by both parties at the end of 2016 (with, as already mentioned, a difficult closing phase), but still has to be ratified. Other countries, too, are contracting bilateral and regional trade agreements. A group of 12 Asian nations and the US negotiated for years on the aforementioned TPP, but since the election of Trump, this is now up in the air. However, this does not mean the end of regional trade agreements; China (which was previously excluded from the TPP) has already stated that it would be willing to take over the role of the US in the TPP and other countries have also already expressed an interest. Although, for many different reasons, many of these negotiations prove difficult, they nevertheless indicate a trend towards regionalisation of trade agreements which will probably continue in the future.

The crucial question is whether the proliferation of bilateral and regional trade agreements constitutes a threat or an opportunity for the multilateral trade regime. On the one hand, regional trade agreements are increasingly being contracted in conformity with the WTO and can serve as a basis for future multilateral negotiations, but at the same time, they also increasingly contain provisions that go beyond the current WTO mandate (e.g. environmental and labour norms).[25] These agreements could hamper WTO regulations in these fields in the future, because different agreements are reached, with no umbrella agreement, and thus represent a threat to the multilateral system. In addition, the issue is not only the content of the agreements, but also the question with which countries these new treaties will or will not be concluded. TTIP and TPP exclude or excluded important (emerging) powers, such as China, Russia, India and Brazil. It is not very realistic to expect that these countries will accept rules at a later stage that they have not drawn up themselves. Trade agreements are therefore not only concluded for economic reasons, but also for geopolitical reasons: efforts are made to form the strongest possible blocs, within which the members’ own norms and rules can apply, in order to be able to present a counterweight to other trading blocs. This is contrary to the principles of the multilateral system, in which the interests of all states, including less well-developed ones, are protected. In this way, the EU and the US, and also China, are pursuing a policy that in itself could constitute a threat to the multilateral trade system, without this necessarily being the intention.[26]

The quadrant chart and shocks

What do these developments mean for the future free trade regime (see Figure 6)? In 2016, there is still agreement on the key norms and rules within the free trade system. Although some norms are under pressure, free trade is still the most important norm of the system. Because all parties have an interest in free trade, including the emerging powers, this is expected to remain the case in the future. However, new rules are no longer drawn up within a multilateral framework (think of the impasse within the WTO), but in other, non-inclusive alliances. In the coming five years, a further shift is expected towards less cooperation and increasing non-compliance with the rules, for example through more frequent deployment of protectionist measures.

In terms of actors, it is no longer only the major powers that determine the agenda and conclude the agreements (as was the case after the Second World War), but increasingly, a larger group of emerging (non-Western) powers. The stagnation of the Doha round, in which the US and the EU no longer have the dominance to smooth over these negotiations, as was the case in earlier rounds, is a sign of the growing importance of the emerging powers. The fact that the established order and the emerging powers come together within the G20, which has replaced the G7/8 as the most important forum, shows that the important decisions are no longer taken by a handful of major powers.

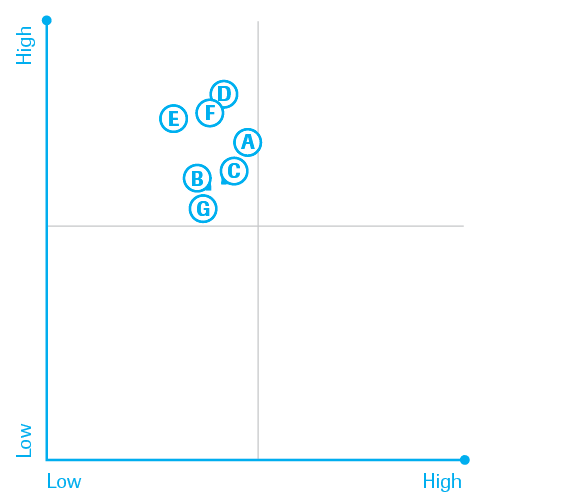

Are developments (‘shocks’) conceivable that could significantly change the assessment of the position of the free trade regime in 2021? This question was put to experts in the fields of trade and economics in the Clingendael Expert Survey. The experts refer to the risk that the US will take a hard isolationist attitude (although they do not consider this very likely) (see Figure F). However, the risk does seem to have become more probable with the election of Trump as president. In that case, cooperation within the world trade system will become even more difficult, lead to even more formation of blocs and to the deployment of more protectionist measures (not only by the US but also by other countries) and will confirm the previous assessment of the international system.

Shock

Conclusion

A number of important trends, such as the stagnation of world trade, new forms of regionalisation, increased protectionist measures and the halt to internationalisation of value chains, etc., will have an impact on world trade in the coming years. These trends present the multilateral system with a challenge. However, in an increasingly multipolar world, strengthening the multilateral trade system on the basis of common rules has proved difficult, as shown by the slow progress of the Doha round. Trade rules are increasingly drawn up on a regional or bilateral basis and place further pressure on the multilateral system.