Misery loves company: Iraq and Iran's electricity and gas dependencies

- The common narrative – mostly US – is that Iraq’s critical dependency on Iran’s electricity and gas exports are a manifestation of Iran’s economic dominance of Iraq while also enabling Iran to circumvent US sanctions

- In contrast, this blog post demonstrates that Iran and Iraq are mutually dependent on these exports/imports. This is not due to any grand design, but rather to similar economic management failures

- If the US were to revoke its current waiver to Iraq that allows the import of Iranian gas - in addition to the already revoked waiver that used to enable electricity imports - it is more likely that Iraq will experience a major energy crisis than that Iran will experience greater financial pressure

By Ahmed Tabaqchali

Editors’ introduction

In September 2022, the death of Mahsa Jina Amini marked a major turning point for Iran. The event sparked lengthy nationwide protests across socio-economic classes and population groups whose demands rapidly evolved from discarding controversial hijab regulations to calls for the overthrow the Islamic Republic. The Iranian government responded with repression, killing over 400 protesters in late 2022 and early 2023, according to human rights groups.

The Clingendael blog series ‘Iran in transition‘ explores power dynamics in four critical dimensions that have shaped the country’s transformation since: state-society relations, intra-elite dynamics, the economy, and foreign relations. This blog post critically assesses the assumptions underpinning US sanction waivers to Iraq regarding the import of Iranian gas and electricity. Specifically, it argues that underlying economic realities render these waivers ineffective as instrument of US pressure on Iran and that their revocation is more likely to cause energy supply problems in Iraq.

The premises underpinning US waivers for Iranian gas and electricity export to Iraq

In early March, the US rescinded the sanctions waiver that allows Iraq to import electricity from Iran while extending its waiver for the import of natural gas. These waivers were introduced by the first Trump administration as part of its maximum pressure campaign against Iran. Their aim was to encourage – or force – Iraq to gradually become energy independent of Iran with regards to gas and electricity. The origins of these sanctions lie in the US narrative that Iran has been the true beneficiary of its 2003 invasion of Iraq and that Iran dominates both Iraq’s economy and its politics. As part of this narrative, Iraq’s import of Iranian electricity and gas is taken to manifest Iran’s economic dominance of Iraq while also enabling it to circumvent US sanctions. The narrative also holds that this state of affairs must come to an end by weaning Iraq off Iranian electricity and gas.

This blog challenges the assertion that this critical dependence is the result of Iranian designs to execute a long-term strategy to establish economic dominance.[i] In doing so, it builds on the arguments already made in the author’s “Big bad wolf, or is it? Iran’s economic footprint in Iraq in context” and in Madi Ghodsi’s “Dark comedy or tragedy? The dire straits of Iran's economy”, which appeared earlier in this series. In the case of Iraq, the state’s chronic management failure of the electricity sector and its mismanagement of resources, which is aggravated by a large and growing gap between domestic demand and domestic supply, leaves it with no other choice but to import electricity and gas, thus creating a major dependency. The reason Iran is Iraq’s top provider in both areas is the close proximity of existing grids, pipelines and major urban centres. In the case of Iran, its gas and electricity exports to Iraq are a rare case of success in view of the overall failure of its energy export strategy. Yet, this success is enabled by Iraqi failures rather than Iranian savviness.

Zooming out: Failures of Iran’s strategy to become a major gas exporter

Iran’s enormous natural gas reserves - 17.1% of the world’s total proven gas reserves - makes it a potential gas super power along with Russia at 19.9%, Qatar at 13.1%, Turkmenistan at 7.2% and the US at 6.7%. In 2020, this quintet accounted for 64% of the world’s total proven reserves. Iran’s strategic location, shortages of gas supplies among its neighbours (Qatar excepted) and Asia’s increasing demand for gas over the last decades, make the country a major potential supplier to both the region and Asia, which can rival Qatar. Finally, Iran could have become an alternative, although secondary, supplier to Europe, filling part of the gap caused by the halt of Russian gas exports to Europe after the invasion of Ukraine.

By 2013, Iran had ambitious plans for the development of its natural gas fields. It had signed Memoranda of Understandings (MoU’s) for pipeline exports with almost all of its neighbours, as well as with India via Pakistan, in addition to plans for gas exports to Europe via Turkey for an envisaged total of 53-56 billion cubic meters (BCM) a year. Additionally, Iran planned to develop its infrastructure for Liquified Natural Gas (LNG) to support further exports of 100-102 BCM a year so as to diversify its export destinations beyond existing pipelines. The plan aimed for a combined export total of 153 - 158 BCM (pipeline plus LNG). Finally, Iran had plans for capturing flared gas, a by-product of oil production.

However, a decade later few of these plans had truly moved beyond the drawing board and those that had, fell short of projections. The next paragraphs review each objective to gauge progress between 2013 and 2023, i.e. a) the number of MoU’s for gas exports by pipeline that became implemented contracts; b) the development of LNG infrastructure and level of export; c) the level of gas flaring.

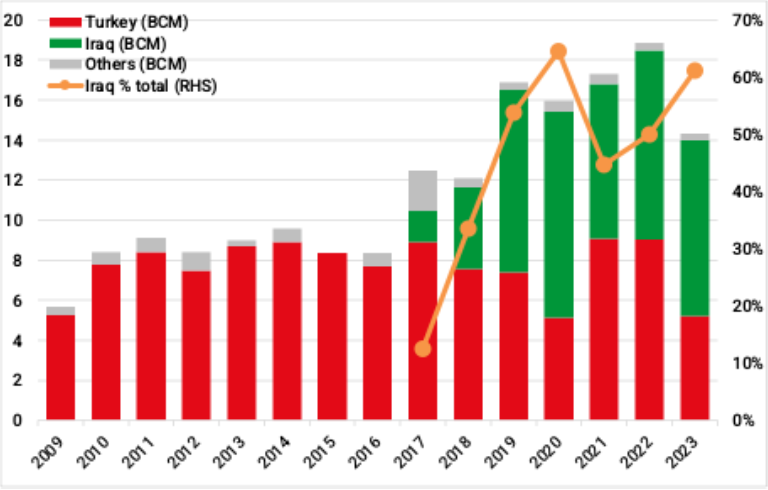

Actual implemented contracts included 1) those with Iraq (discussed below; green bars in Figure 1), 2) swap contracts with Armenia and Azerbaijan in which Iran exported gas and imported gas or electricity (these averaged 0.6 BCM between 2009 and 2023; see the grey bars in Figure 1), and 3) exports to Turkey (5.3 BCM in 2009, growing unevenly to 9.08 BCM in 2021 and then declining to 5.2 BCM in 2023 while Turkish domestic consumption grew from 33.7 BCM to 48.4 BCM (+43.6%), see red bars in Figure 1). In brief, most MoU’s Iran had concluded with its neighbours by 2013 were still words on paper a decade later. Figure 1 provides total Iranian gas exports by pipeline to Armenia, Azerbaijan, Turkey and Iraq.

Figure 1: Iran gas exports between 2009 and 2023 to Turkey, Iraq and Armenia/Azerbaijan (‘others)

Sources: see end of the blog, RHS means ‘Right Hand Side’, i.e. indicating the scale on the vertical axis to the right side of the Figure.

Moreover, while Iran’s LNG infrastructure developed somewhat, the country neither became an LNG producer nor an exporter although it remains hopeful that some of its plans will come to fruition in 2026. By 2023, Iran had pipeline exports of 14.3 BCM, made up of 8.8 BCM to Iraq, 5.2 BCM to Turkey, as well as 0.4 BCM in exports to Armenia and Azerbaijan, but no LNG exports. By comparison, each of the other members of the quintet of major gas powers had exports that dwarfed Iran’s: Russia exported 42.7 BCM and 95.4 BCM in LNG and pipeline volumes respectively, Qatar 108.4 BCM and 19.5 BCM in LNG and pipeline exports, Turkmenistan had 39.5 BCM pipeline exports, and the US had 114.4 BCM and 89.1 BCM in LNG and pipeline exports. Finally, Iran ranked second in the world behind Russia in gas flaring in 2023. Industry data show that its flaring levels in that year were only slightly less than during the ‘flaring high’ of 2022.

In short, Iran’s strategy to turn its gas potential into a source of regional influence (akin to Russia before its invasion of Ukraine in 2022) and a source of hard currency earnings remains aspirational at best and a managerial failure at worst. Iran’s broader failure to develop and manage its enormous potential as a gas and electricity exporting powerhouse contradicts the very idea that it is capable of executing a strategy to dominate Iraq’s economy via these sectors. While sanctions played a major part, Iran’s management failures are also embedded in its political economy, notably the existence of parallel religious and statal decision-making structures, high levels of corruption, and technology shortcomings.

Zooming back in: Surprising success in Iran’s gas exports to Iraq

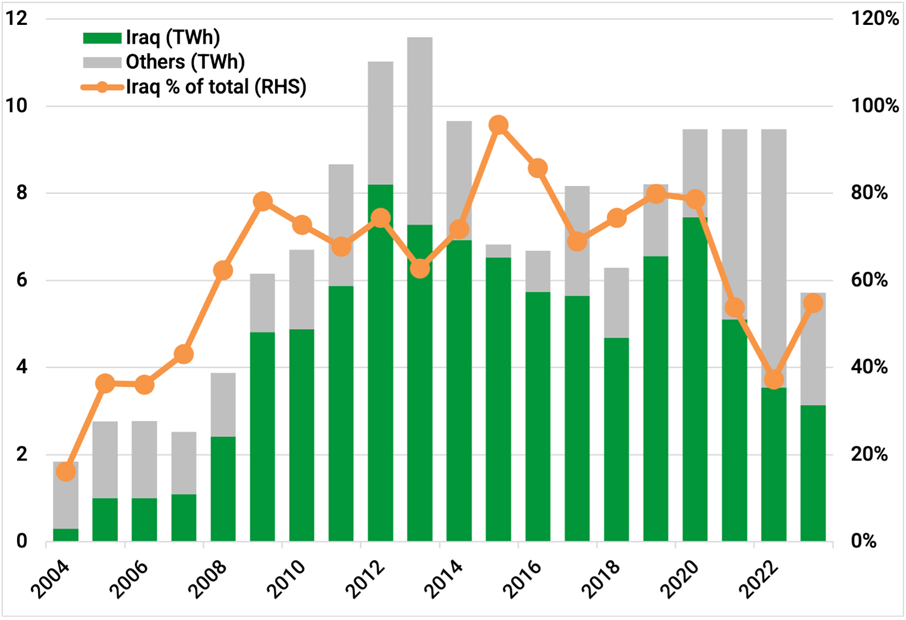

To begin with, it is useful to note that even though gas exports from Iran to Iraq are meaningful and create significant Iraqi dependency – and hence Iranian influence – they are a shadow of initial ambitions. In 2023, Iranian gas accounted for 47% of Iraqi domestic gas consumption, which is used to generate an estimated 29% of Iraqi electricity generation. Plans for Iranian exports to Iraq date back to 2011 and were much more substantial than what came to pass. An initial MoU anticipated the building of a 40 BCM pipeline that would run through Iraq, Syria, Lebanon and through the Mediterranean to Europe. Around 24 BCM was earmarked for Europe and 16 BCM for Iraq and Syria. This ended up in 2013 as a contract to export up to c. 18 BCM a year, which has not even been delivered as billed despite Iraqi demand for gas increasing since 2013. Exports in fact only started in the summer of 2017, steadily grew until 2020 and peaked at c. 10 BCM (c. 57% of contracted supply). By 2023, this volume had declined by 14.9% to c. 9 BCM while total Iranian gas exports declined by c. 10% (Iranian gas production was up 6.7% during this period). Iranian electricity exports to Iraq did not develop in any meaningful way either. This is largely because the increase in gas production in Iran did not keep up with the much faster increase in domestic electricity consumption, which requires gas to be generated, as well the increased demand for gas for heating. Iranian electricity exports to Iraq started in 2004, peaked in 2012 and declined afterwards (see Figures 2 and 3).

Figure 2: Iranian electricity exports between 2004 and 2023

Sources: see end of the blog, TWh is Terawatt hours, RHS means ‘Right Hand Side’, i.e. indicating the scale on the vertical axis to the right side of the Figure.

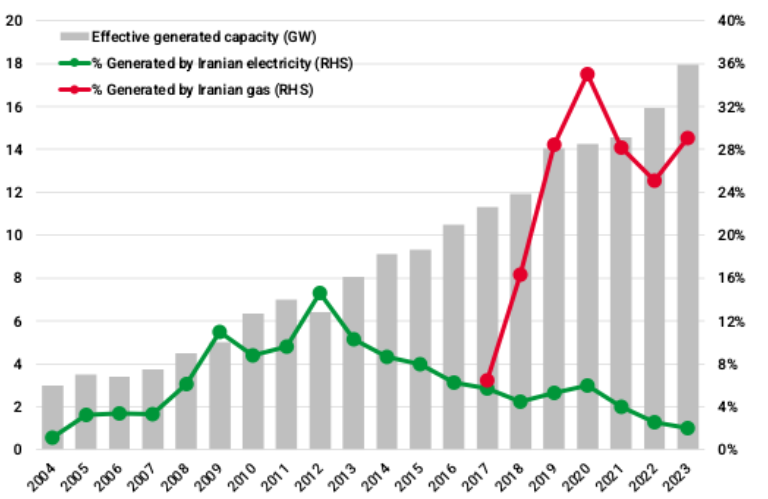

Regardless of the decrease in Iranian gas and electricity exports to Iraq, Iran remains an essential supplier, as Figure 3 for example shows. In 2023, Iran provided about 31.0% of Iraq’s electricity. On the other hand, the high percentage of gas/electricity exports to Iraq of Iran’s total gas/electricity exports (Figures 1 and 2) also shows Iran’s dependence on Iraq as a market for its gas/electricity exports, especially in view of the failure of its broader export strategy noted above. In an odd sort of way, Iranian gas/electricity exports – and any associated projection of soft power – are highly dependent on Iraq.

Figure 3: Iran’s contribution to Iraqi electricity supply

Sources: see end of the blog, GW is gigawatt, RHS means ‘Right Hand Side’, i.e. indicating the scale on the vertical axis to the right side of the Figure.

Similar structural impediments to development

Iraq’s dependency on Iran to meet its gas/electricity demand and Iran’s dependence on Iraq as a market for its exports of gas/electricity are the result of similar structural shortcomings. As to Iraq, failings in the management of every aspect of its power production infrastructure have been apparent for years – from the power plants that generate electricity to the transmission system that transports this electricity to population centres and the distribution networks that channel electricity to end users. Compounding these management failures is a mix of dysfunctional tariff pricing and a collection system that encourages unlimited consumption, poor coordination between the Ministries of Electricity and Oil leading to the mis-provisioning of the appropriate fuels for power generation. It is this collection of policy and managerial failings that has prevented Iraq from increasing its own gas production and diversifying its supplier portfolio.

As to Iran, its gas and electricity production infrastructure have been woefully mismanaged, resulting in both a lack of maintenance and a lack of upgrading, wasteful government subsidies that encourage unlimited consumption and underinvestment in aging infrastructure aggravated by sanctions. This has caused demand for electricity and gas to outstrip supply to an extent that exports have had to be diverted to the domestic market during peak months, at times causing breaches of contract. In 2024, this gradual worsening state of affairs was accelerated by weather extremes in both summer and winter, developed into a full blown crisis with power blackouts across the country.

In brief, Iran’s success in exporting electricity and gas to Iraq, in comparison with its other export plans, has more to do with Iraq’s economic dysfunction and supply needs than with Iranian economic brilliance. The reason Iran nevertheless ended up in a dominant position is due to the extensive land border between the two countries and the proximity of Iraq’s most densely populated urban areas to Iran, which makes it relatively straightforward to build infrastructure for the export and delivery of electricity and gas.

The likely impact of waiver revocation

The inherent contradiction of US sanction waivers issued to Iraq is that they are short to medium-term provisional measures that allow Iraq to meet its energy needs whereas implementing realistic plans for achieving Iraqi energy security requires a long-term effort. It is therefore not a surprise that the waivers have not achieved their intended result in the relatively short period since they were first initiated. To be an agent of real and lasting change, they would need to be accompanied by joint consultations and collaboration about the design and implementation of an Iraqi diversification strategy for its gas and electricity supply. Right now, their revocation will only jeopardize Iraq’s energy security, leading to socio-economic problems in Iraq more than exerting financial pressure on Iran.

It is useful to bear in mind that Iraqi payments for imports from Iran are not made directly to Iran, but are deposited in monitored bank accounts. Such payments were held at the Trade Bank of Iraq (TBI) until recently, but since the summer of 2023 they have been deposited into similar restricted accounts at third-country banks with US agreement. The use of these funds is limited to humanitarian and other non-sanctioned purposes, and overseen by the US Treasury. Such controls do not fully exclude abuse, but put paid to the notion that the formal trade somehow generates significant resources that are freely available to Iran.

Achieving energy security requires Iraq to diversify its sources of electricity supply and of gas for the generation of electricity, and not simply replacing Iranian electricity and gas imports. The challenge for Iran is rather to develop its enormous gas reserves so that its production can meet both domestic electricity consumption and generate export earnings. However, this cannot be done without major transfers of foreign technology and knowhow. In other words, it requires the end of sanctions and reconnecting Iran to the global world of investment. It is here that the US has real leverage over Iran, by offering investment and knowhow, rather than threatening the revocation of sanctions that are likely to hit Iraq harder than Iran, and give Iran a convincing story to blame the US for any ensuing hardship.

Read earlier blogs in this series.

[i] The research in this blog post on Iran’s gas development plans, is based on “Iran’s gas exports: can past failure become future success?” which, in addition to data on gas plans, provided insight into the interplay of Iran’s political economy and gas development plans.

Notes on data used in piece and charts: Author’s calculations and estimates based on gas and electricity data were sourced from the Energy Institute “Statistical Review of World Energy for 2024”, Iraq’s Ministry of Electricity annual reports 2010-2023; Iran’s Tavanir Holding Company “Statistical Report on 49 Years of Activities of Iran Electric Power Industry (1967-2015)”, and US’s Energy Information Agency’s (EIA) Iran data. Iran tends to report its data using Iranian fiscal years which end in March, but it’s not clear whether the data Iran provides to international agencies is adjusted for this, and so actuals may differ slightly in a given year from those used in the calculations underpinning this blog.